+91 6002993949

submission@himjournals.com

Open Access

ISSN (Print) : 2709-3549

ISSN (Online) : 2709-3557

The accounting profession in Malaysia is facing problem where the demand for accountants is higher than the number of accountants produced. The accounting education need to be nurtured from the early stage of education. The objective of this study is to investigate factors influencing students’ intention to choose accounting as their major academic program after graduating from secondary/high school. 113 questionnaires were collected from secondary school students in Northern Region of Malaysia. Using a Theory of Planned Behavior, the result show that attitude towards accounting program (ATT), subjective norm (SN) and perceived behavior control (PCB) have significant positive relationship with students’ intention to enroll in accounting program. To increase numbers of accountants in the industries, the government through Ministry of Education (MOE) should pay more attention and collaborating with professional bodies, audit firm and higher-level education institution in motivating secondary school students and create positive perception toward accounting courses and fields among them.

Under Malaysia Economic Transformation Program, Malaysia has put a target to produce 60,000 accountants by 2020 and in year 2019, it was reported that there are more than 35,000 qualified accountants in Malaysia registered with Malaysia Institute of Accountant (MIA) [1]. This number is quiet far to reach the target set. A collaborative effort from the accountancy profession, government and organizations are required to increase number of accountants, to encouraged and nurtured a good and positive attitude toward accounting among students. This effort needs to start from early stage of education. Albrecht & Sack [2] reported that accounting program experienced a drastic reduction in the number of students’ enrolment. They identified few reasons that cause reduction of accounting graduate, such as the nature of accounting subjects, the risky future of the program and the accounting profession, and perception toward corporate scandals. Furthermore, as reported by Zakaria et al. [3] accounting is perceived as non-interesting subject, difficult, and hard to understand. Past studies also show that personal interests, peer influence, family background, career opportunity and job availability are among factors that influence students’ decision to major in accounting program [3,4]. Contradictory with Rababah [5], his study revealed that personal interests, personality, job prospect and reputation, and media did not have significant influence on the students’ choice of accounting as a major. These previous studies have led to inconclusive finding on the influencing factors. A proper plan to attract more students to enroll in accounting program should be one of the agenda that need to be considered by government. Thus, this study explores factors that might influence secondary school students to pursue accounting program in their tertiary level education. This study is based on the theory of planned behavior and the factors are classified into three categories: attitude toward accounting program (ATT), subjective norms (SN) and perceived behavioral control (PCB).

Literature Review

Theory of Planned Behavior: Theory of planned behavior (TPB) refines the theory of reasoned action (TRA) by including the concept of perceived behavioral control. Theory of reasoned action (TRA) by Ajzen and Fishbein [6] provides a social psychological framework that is beneficial in explaining the behaviors or actions. According to TRA, the immediate determinant of the theory is the intention. The TRA holds two independent determinants of intention, which are attitude and subjective norm. The attitudes are made up of a person’s salient beliefs that the action leads to certain outcome, it can be either positive or negative [3]. While subjective norms refer to the belief that an important person or group of people will approve and encourage the behavior [7]. The relationship between the two independent determinants (attitude and subjective norm) and immediate determinant (intention) are positive. It means that the higher the attitude and subjective norm, the higher the intention to perform a behavior.

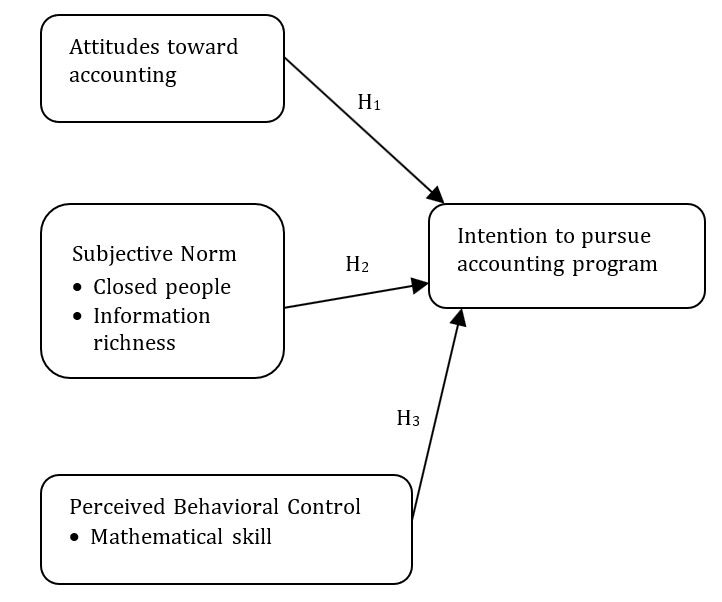

Figure 1: Research Framework

Meanwhile, perceived behavioral control refers to one’s perception of his/her ability to carry out a certain behavior or action. The relationship between the perceived behavioral control and intention to perform a behavior is positive. It means that the higher the perceived behavioral control, the higher the intention to perform a behavior. In other words, the more ability one believes he/she has, the higher intention to perform the behavior. Normally, it is hard to determine the actual behavior of a person. This is because there are many factors that might affects the intention of a person to perform a behavior. This study used TPB which consist of attitude toward accounting, subjective norm, and media richness information on accounting and perceived behavior control on students’ ability and her/his skill in mathematical subject as independent variables and intention to pursue accounting program/field as dependent variable. The research framework is illustrated in figure 1.

Attitudes toward Accounting

Attitudes are made up of a person’s salient beliefs that the action leads to certain outcome, it can be either positive or negative [3]. Attitudes are one of the significant factors that influence student intention to enroll to a program. The decision of student major is significantly influenced by the career opportunities, prestige of the profession and high pay from the profession [8-13]. These motivation factors differentiated the attitudes into extrinsic and intrinsic. According to Porter & Woolley [14], extrinsic attitudes include high earnings, advancement potential as well as high job availability. While the intrinsic attitudes include enjoyable course work, exciting career, and accounting as interesting subject. Results from these studies show that extrinsic and intrinsic attitude has significant influence on the students’ intention to choose a program. In addition, Yusri et al. [15] also reveal that attitude towards accounting significantly influence students’ intention to pursue accounting program/fields. However, Dalci et al. [16] in their study found that intrinsic factors such as interest in the subject and perception towards accounting course do not significantly influence students' decision. The same finding also being reported in Rababah [5], who found that personal interests, personality, job prospect and reputation do not have significant influence on the students’ choice of accounting as a major. Thus, there were mixed results from previous studies on the relationship between attitude and intention of students accounting. As such, this study hypothesizes that:

H1: Attitude towards accounting significantly influence students’ intention to pursue accounting program/fields.

Subjective Norm (SN)

Subjective norms refer to the belief that an important person or a group of people will approve and encourage one behavior [7]. In other words, it means that people who are closed with a person can influence the person action and decision. Generally, in this contact of study, the subjective norm includes parents, siblings, teacher, friend, advisor, and peers. These group of people are important and can influence students’ future decision regarding their study. From previous research, most of studies concluded that subjective norm has significant influence on student’s intention to enroll/pursue accounting program/feilds [3,4,17]. However, Alanezi et al. [8] found that friends and family advice were the least important factors in the students’ decision as compared to attitude and perception toward accounting as an interesting subject, give high earning, career opportunity and prestige profession. This finding was also reported by Sharifah and Tinggi [18] where they found that parents’ influence did not affect the students’ decision. Becker and Gibson [19] also found that subjective norms do not influence the intention to enroll in a Bachelor of Accounting program in United States. United States students are more independent when choosing their major rather than rely on the view of others. Most of these studies have shown a mixed results on the relationship between subjective norms and intention. As such, this study hypothesizes that:

H2a: Closed people significantly influence students’ intention to pursue accounting program/fields.

Information Richness

The amount of information is another independent variable examined by several research [4,20-22]. In digital technology era, students get information about accounting field of study from internet, social media, newspapers, radios, and TV program. Students in the digital era usually search information through website, search engine and many other channels about universities and colleges for courses offered and the potential fields. According to Hanudin et al. [20], the amount of the information is one of the factors that influence the intention of students’ in Universiti Malaysia Sabah (UMS) to enrol in accounting program. According to Macionis et al. [21] and Andrews [22] media in the form of television, advertisement and the internet give impact on the behaviour of students. Subsequently, based on the over discourse, this study hypothesizes that:

H2b: Information richness significantly influences students’ intention to pursue accounting program/fields.

Perceived Behavioral Control (PBC)

Perceived behavioral control refers to one’s perception of his/her ability to carry out a certain behavior or action. The relationship between the perceived behavioral control and intention to perform a behavior is positive. Generally, the perceived behavioral control includes previous achievement and ability of a person. For example, those who excel in playing with numbers or those who are good in mathematics would consider choosing accounting as a major. According to Kim et al. [23] study that focused on the perception of the non-accounting student and accounting student on accounting program in Ton Duc Thang University, Vietnam, reported that both group of students agreed that learning accounting as major has less pressure and accounting major is suitable for people that good in numbers. Meanwhile, Porter & Woolley [14] reported that students will proceed to continue study in accounting related fields, when they meet the math requirement and success in introductory accounting course. The findings show that the perceived behavioral control such as, skill on math [14], good understanding, good in grammar [24], good academic performance [25] have significant influence on students’ choice of major. As such, this study hypothesizes that:

H3: Mathematical skill significantly influences students’ intention to pursue accounting program/fields

Data Collection

This paper aims to examine factors affecting secondary school students to pursue accounting programs at university level. A survey type method was used for this study. Online questionnaires were distributed to secondary school students studying in form 4, form 5 and form 6 in National Secondary Schools at Northern region of Malaysia. Operational variables in this study are divided into attitudes toward choosing the accounting program, Closed people and information richness under subjective norm category and mathematical skilled as independent variables and intention pursue accounting program/field as dependent variables. All these variables were measured with five statements using a 5-point Likert scale ranging from strongly disagree to strongly agree. A total of 113 questionnaires were collected and usable for data analysis.

Descriptive Analysis

As shown in Table 1, from 113 respondents, 77 are female students and 36 males and 50.5% are in form 4 and form 5 who will be taking Sijil Pelajaran Malaysia (SPM) and 49.5% are in form 6 who will be taking Sijil Tinggi Pelajaran Malaysia. 60.2% taking accounting subject, comes from the Art Stream and Social Science discipline. While 39.8% respondents did not take accounting subject comes Science Stream and other discipline. The frequency of Malay and Chinese students is the highest compared to Indian and other students, which are 42 Malay and 48 Chinese students compared to 23 Indian and other race students.

Reliability test

Reliability test was run for all the 4 variables: attitude, subjective norm, perceived behavior control, and

Table 1: Respondent’s profile

| Year of study | Frequency | Percent | Discipline | Frequency | Percent |

| Form 4 | 21 | 18.6 | Art | 56 | 49.6 |

| Form 5 | 36 | 31.9 | Social Science | 12 | 10.6 |

| Lower 6 | 37 | 32.7 | Science | 29 | 25.6 |

| Upper 6 | 19 | 16.8 | Other | 16 | 14.2 |

| Total | 113 | 100 | Total | 113 | 100 |

| Ethnicity | |||||

| Race | Frequency | Percent | Accounting Subject | Frequency | Percent |

| Malay | 42 | 37.2 | Yes | 68 | 60.2 |

| Chinese | 48 | 42.5 | No | 45 | 39.8 |

| Indian | 17 | 15 | Total | 113 | 100.0 |

| Others | 6 | 5.3 | |||

| Total | 113 | 100 | |||

| Sex segmentation | |||||

| Gender | Frequency | Percent | |||

| Male | 36 | 31.9 | |||

| Female | 77 | 68.1 | |||

| Total | 113 | 100.0 | |||

Table 2: Reliability Statistics

| variables | Cronbach's Alpha |

| Attitude | 0.804 |

| Closed people | 0.837 |

| Information richness | 0.788 |

| Mathematical skill | 0.896 |

| Intention | 0.948 |

Table 3: Multi-Regression: effect of attitude, subjective norm and mathematical skill on intention to pursue accounting major

| Model | Beta Coefficients | Std. Error | t | Sig. P value | Collinearity Statistics VIF |

| (Constant) | -0.249 | 0.179 | -1.386 | 0.166 | - |

| Attitude | 0.319 | 0.105 | 3.020 | 0.003 | 5.138 |

| Closed people | 0.185 | 0.080 | 2.320 | 0.022 | 2.946 |

| Information richness | 0.054 | 0.043 | 1.248 | 0.215 | 1.393 |

| Mathematical skill | 0.520 | 0.075 | 6.963 | 0.000 | 3.453 |

| Adjusted R Square | 0.814 | ||||

| F value | 123.556 | ||||

| Sig. | 0.0000 | ||||

intention variables. Table 2 below shows the results of Cronbach's Alpha for all the variables. A Cronbach’s alpha coefficient of 0.7 or higher is considered acceptable by most social science researchers. In this study, the Cronbach’s alpha coefficient for all the four variables were above 0.8, thus indicating the overall reliability for the measurement.

Regression Analysis

To test the influencing factor on students’ intention to pursue accounting program in their Tertiary Level Education, multiple regression analysis was carried out as shown in Table 3 below. Multi-Regression analysis from the table revealed that attitude, subjective norm and mathematical skill are significant to students’ intention with P value is less than 0.05. The results are same as the previous research [3,4,14] that reported attitude, subjective norm and perceived behavior control have significant influence on the students’ intention. Although there are some of the previous researches mentioned that subjective norm does not necessarily influence on the students’ intention to choose a program [8,19] but the results in this study proved that people who closed to students have significant influence on their intention to choose accounting program as their major. As for information richness, the result shows that this factor has no significant relationships toward students’ intention. This results however was contradict from study done by Macionis et al. [21] and Andrew [22] which stated that media in the form of television, advertisement and the Internet give the impact on the behavior of students. The regression model also fit with adjusted R2 equal to 81.4% which means that all the three variables (attitude, subjective norm and mathematical skill) could explain 81.5% students’ intention to pursue accounting program in their Tertiary Level Education except for information richness. On the other hand, the remaining 18.6% of the dependent variables can be indicated by other factors that not included in the model since there are not all the variables or factors are being used in this research.

This study investigates factors that influence students’ intention to enroll in accounting program. Factors being studies were students’ attitude toward accounting, subjective norm, information richness and perceived behavior control specifically on the mathematical skill of the students. Based on result of descriptive analysis, most of the students have positive attitude towards choosing accounting program. Specifically, the findings of the study reveal that these factors significantly related to students’ intention towards accounting program except for information richness factors which was not significant. This implies that the intention to pursue accounting program at tertiary level of education should be emphasized at the early stage of education and motivation and encouragement from people who are closed with the students. Even though information richness was found not significant in this study, past literature result cannot be denied. Thus, the relevant organizations need to play their role in conveying information to young students in order to increase and cultivate interest on accounting subject to achieve expected number of accountants in the country.

Yee, Wee Peng. "Turning Malaysia into a global accountancy hub." The Star, 11 Oct. 2019. https:// www. thestar. com.my/ business/ business-news/ 2019/ 10/ 11/ turning- malaysia- into- a- global-accountancy-hub. Accessed 6 Oct. 2020.

Albrecht, W.S. and R.J. Sack. Accounting Education: Charting the Course Through a Perilous Future. Accounting Education Series, vol. 16, American Accounting Association, Sarasota, FL, 2007, pp. 603–611.

Zakaria, M. et al. "Accounting as a choice of academic program." Journal of Business Administration Research, vol. 1, no. 1, 2012, pp. 43–56.

Zandi, G., B. Naysary and S.K. Say. "The behavioral intention of Malaysian students toward accounting discipline." Accounting and Management Information Systems, vol. 12, no. 3, 2013, pp. 471–488.

Rababah, Abedalqader. "Factors influencing the students’ choice of accounting as a major: The case of X University in United Arab Emirates." International Business Research, vol. 9, no. 10, 2016, pp. 25–32.

Ajzen, Icek and Martin Fishbein. Understanding Attitudes and Predicting Social Behavior. Prentice-Hall, Englewood Cliffs, New Jersey, 1980.

Ham, Maja, M. Jeger and A. Frajman. "The role of subjective norms in forming the intention to purchase green food." Economic Research-Ekonomska Istraživanja, vol. 28, no. 1, 2015, pp. 738–748.

Alanezi, F.S., M.M. Alfraih and A.E. Haddad. "Factors influencing students’ choice of accounting as a major: Further evidence from Kuwait." Global Review of Accounting and Finance, vol. 7, no. 1, 2016, pp. 165–177.

Odia, J.O. and K.O. Ogiedu. "Factors affecting the study of accounting in Nigerian universities." Journal of Educational and Social Research, vol. 3, no. 2, 2013, pp. 89–96.

Ahinful, G.S., R.O. Paintsil and J.B. Danquah. "Factors influencing the choice of accounting as a major in Ghanaian universities." Journal of Education and Practice, vol. 3, no. 15, 2012, pp. 101–105.

Tan, L.M. and F. Laswad. "Students’ beliefs, attitudes and intentions to major in accounting." International Journal Accounting Education, vol. 15, no. 2, 2006, pp. 167–187.

Lowe, D.R. et al. "Criteria for selection of an academic major: Accounting and gender differences." Psychological Reports, vol. 75, 1994, pp. 1169–1170.

Galotti, K.M. and S.F. Kozberg. "Older adolescents’ thinking about academic, vocational and interpersonal commitments." Journal of Youth and Adolescence, vol. 16, no. 1, 1987.

Porter, J. and D. Woolley. "An examination of the factors affecting students’ decision to major in accounting." International Journal of Accounting and Taxation, vol. 2, no. 4, 2014, pp. 1–22.

Yusri, Y., C.Y. Ooi, R. Mohd Said and N.I. Mahyuddin. "Attitude toward accounting: A study among secondary school students in Malaysia." Himalayan Journal of Economics and Management, vol. 2, no. 99, 2021, pp. 76–81.

Dalci, İlhan et al. "Factors that influence Iranian students’ decision to choose accounting major." Journal of Accounting in Emerging Economies, vol. 3, no. 2, 2013, pp. 145–163.

Mazzarol, Tim and Geoffrey Soutar. "Push-pull factors influencing international students’ destination choice." The International Journal of Educational Management, vol. 16, no. 2, 2002, pp. 82–90.

Sharifah, S.S. and M. Tinggi. "Factors influencing the students’ choice of accounting as a major." The IUP Journal of Accounting Research & Audit Practices, vol. 12, no. 4, 2013.

Becker, E.A. and C.C. Gibson. "Fishbein and Ajzen's theory of reasoned action: Accurate prediction of behavioural intentions for enrolling in distance education courses." Adult Education Quarterly, vol. 49, no. 1, 1998, pp. 43–56.

Hanudin, Amin, A.R. Abdul Rahim and T. Ramayah. "What makes undergraduate students enroll into an elective course?" International Journal of Islamic and Middle Eastern Finance and Management, vol. 2, no. 4, 2009, pp. 289–304.

Macionis, John J., Cecilia Benoit and Mikael Jansson. Society: The Basics. Prentice Hall, Upper Saddle River, NJ, 2000.

Andrew, Lisa L. How to Choose a College Major. The McGraw-Hill Companies, Inc., 2006.

Kim, Phan Hoai Vu and Thanh Hoang Chi Thanh. "Factors influence students’ choice of accounting as a major." MSED Conference 2016. https://msed.vse.cz/msed_2016/article/292-phanhoai-vu-paper.pdf. Accessed 28 May 2025.

Savolainen, Hannele, T. Ahonen and M.L. Aro. "Reading comprehension, word reading and spelling as predictors of school achievement and choice of secondary education." Learning and Instruction, vol. 18, no. 2, 2008, pp. 201–210.

Olitsky, Neal H. "Academic achievement and the college major earnings." University of Massachusetts Dartmouth, 2009.