Model Identification

The data obtained were then performed data analysis. The identification of the model is the first thing that must be done. This identification aims to see the problem of heteroscedasticity by using the correlogram test and kurtosis test. The correlogram test can be seen from the value of the Autocorrelation Function (ACF) in the first 15 lags. If the ACF value is not close to zero, then the data has heteroscedasticity. Furthermore, the kurtosis value is also used to identify the problem of heteroscedasticity. If the kurtosis value is more than 3 then the data is heteroscedasticity.

Based on the results of the correlogram test in Table 1, it can be seen that the beef price data in this study has an ACF value that is not close to zero so that it has fulfilled the requirements needed for volatility analysis because it has heteroscedasticity problems. While the kurtosis value of beef price data in this study was 3.054, which means it was greater than 3, then the data had heteroscedasticity problems. Based on the correlogram test and kurtosis test, the data in this study has a heteroscedasticity problem. If the heteroscedasticity requirements have been met, the next stage of analysis can be carried out.

Model Estimation

After the heteroscedasticity conditions are met, the next thing to do is to estimate the ARIMA model. Stationary test using Augmented Dickey Fuller (ADF) is the first thing to do in forming the ARIMA model. If the probability value is less than the 5 percent significance level, it can be concluded that the data is stationary. If the data is still not stationary, differencing will continue until the data becomes stationary. To find out the best ARIMA model, it is done tentatively. The differencing value can describe the d value in the ARIMA model, while the AR (p) and MA (q) values are determined in a tentative way to produce the best ARIMA.

Based on Table 2, it can be seen that beef is not stationary at the 5 percent level of significance. So that the next stationary test is carried out, namely at the first difference stage. The beef data was stationary after the first differencing, so the beef commodity was stationary at the first difference. So it can be continued to find out the best ARIMA model. Based on these results, the value of d is obtained by 1. The values of p and q are determined tentatively. The best ARIMA of beef commodities obtained tentatively is as follows ARIMA (1, 1, 1). After the best ARIMA model is formed, then the ARCH test is carried out which is used to determine the ARCH effect in the ARIMA model that is formed. If the ARCH effect in the model is known, it can be continued to the ARCH GARCH test. The ARCH effect can be seen from the probability value of F statistic which is less than the alpha value of 0.05.

Based on Table 3, the ARIMA model of beef commodities has an ARCH effect so that it can be continued to test the best ARCH GARCH model. Based on the results of the analysis, the best ARCH GARCH model for beef commodities is GARCH (1,2).

Model Evaluation

After identifying the model and model estimation, the next step is model evaluation. In this study, the ARCH LM test was used to determine the ARCH effect was still present in the ARCH GARCH model. If the ARCH effect is no longer in the model, the model is good.

Based on Table 4, the results of the ARCH LM analysis show that the ARCH LM test results obtained are 0.9497. The probability value obtained is greater than the 0.05 level of significance. This shows that the selected model is free from the ARCH effect. So that the resulting model is adequate and meets fulfillet.

ARCH GARCH Model

After the stages to form the model are complete, the ARCH GARCH model of beef is obtained as follows:

Here is the GARCH (1,2) model of beef prices in global markets:

σ2t = 0.00031700604709 + 0.469892802485 e2t-1 + 0.227761279984 σ2t-1 + 0.375790624267 σ2t-2

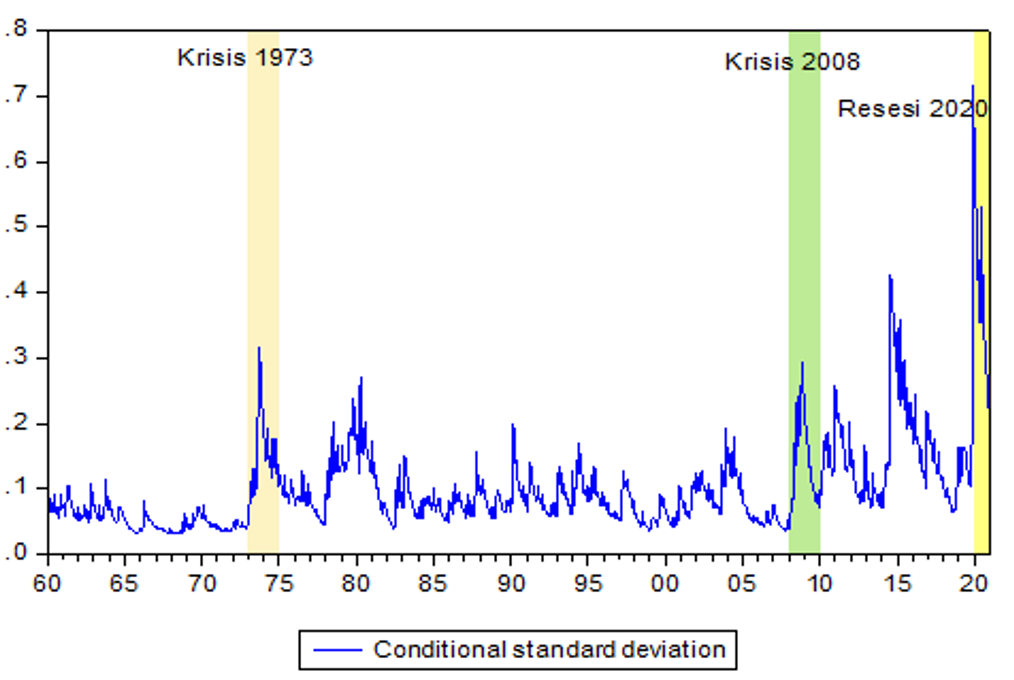

Based on table 4, it can be seen that the beef variance model equation has one ARCH term and two GARCH terms. Furthermore, it can be seen that the variance of beef prices in the world market is influenced by the volatility of beef prices in the previous period. The two GARCH coefficients when added together are 0.604, indicating that the variance shock will affect the price variance in the long term. The conditional standard deviation graph can be used to determine the volatility analysis. The higher the peak of the graph, the more volatile the commodity price will be. The following is a graph of global beef price volatility.

In this study, it is divided into 3 periods, namely the 1973 crisis, the 2008 crisis and the 2020 recession. This is because during these periods there were shocks in the economy. Figure 1 shows a graph of global beef price volatility during the period January 1960 to December 2020. High price volatility can be seen from the high peak of the graph. Beef prices in the 1973 crisis and the 2008 global crisis seemed more stable and less volatile. So it can be seen that the 1973 crisis and the 2008 crisis did not have an effect on global beef prices. Prices in the 1973 crisis and 2008 crisis remained stable because domestic and international supplies were still sufficient so that supply and demand were met. But what is of concern is that the highest volatility occurs in the 2020 recession, namely during the Covid-19 pandemic that spreads in various parts of the world. This is due to production disruptions from exporting countries which are constrained by cattle production due to certain policies during the Covid-19 pandemic. The imbalance between supply and demand causes prices to rise.