The Roles of Attitude, Subjective Norm, And Perceived Behavioural Control in Determining Consumers' Behavioural Intentions Towards Sustainable Banking Services

Jamal Radifan

1

,

Mustika Sufiati

1

,

Mohammad Hamsal

2

1

School of Business and Management, Institut Teknologi Bandung, West Java, Indonesia

2

Management Department, BINUS Business School, Doctor of Research in Management, BINUS University

Sustainable banking is growing in popularity, as sustainable finance practices have gained traction in the global banking sector. To ensure the long-term stability and resilience of the financial sector, banks promote sustainable practices, facilitate the transition to a low-carbon economy, and manage environmental risk. Consumer awareness of social and environmental issues is increasing. This study develops and evaluates a conceptual framework to identify the variables that influence Indonesian customers’ adoption of sustainable banking services. The study gathered data from a cross-sectional sample of 180 respondents through a survey, in accordance with the theory of planned behaviour (TPB). The study model was tested using a structural equation model method based on Partial Least Squares. The results indicate that purchase intention is positively and significantly influenced by attitude and perceived behavioural control. Subjective norms have a positive but insignificant influence, whereas attitude significantly mediates the relationship between purchase intention and subjective norms. This study contributes to the existing knowledge on sustainable customer behaviour in banking and provides guidance to managers and policymakers on how to support sustainable banking practices.

Keywords

Sustainable Banking

Purchase Intention

Sustainability

Customer Behaviour

Theory of Planned Behaviour

Attitude

INTRODUCTION

Financial institutions have become increasingly aware of ESG issues in recent years, particularly in relation to sustainable finance. The term 'sustainable finance' encompasses a wide range of concepts. According to the European Commission [1], sustainable finance is a dynamic process that incorporates environmental, social, and governance issues into financial and investment decisions. Kumar et al. [2] define sustainable finance as all activities and features that promote sustainability in finance. Frameworks for sustainable finance, such as taxonomies for sustainable investment, are being developed to provide guidance for sustainable investment and economic activity. These frameworks can influence the environmental impact of decision-making by promoting a 'significant contribution' and 'do no significant harm' approach towards critical environmental elements [3].

Indonesian financial regulators are increasingly acknowledging the significance of sustainable finance and taking steps to encourage green finance and sustainable funding options. According to Otoritas Jasa Keuangan Regulation Number 51/POJK.03/2017 on the Implementation of Sustainable Finance for Financial Services Institutions, Issuers, and Public Companies, financial institutions must develop a plan that incorporates environmental, social, and governance aspects into their business plans and publish an annual report to the public on how sustainability principles are applied. Banks play a crucial role in promoting sustainable practices due to their unique position as intermediaries. To maintain this role, banks are transitioning towards sustainable or green banking practices. These practices involve offering financial products and services that prioritize sustainability while remaining profitable and meeting the financial needs of customers [4,5].

Consumers are becoming more conscious of environmental and social issues, and this has resulted in changes in the financial industry. To meet changing customer, shareholder and regulatory demands, banks are now expected to provide clear explanations of their approach to managing environmental, social and governance responsibilities, both in their internal operations and in their lending and investment portfolios [6,7]. Banks are placing greater emphasis on sustainability in response to the increasing prevalence of environmental and social challenges worldwide. Sustainable banking has grown in popularity and includes practices such as ethical investment, responsible lending and environmentally friendly operations [8].

The critical factors influencing consumers' intentions to purchase sustainable banking services need to be identified by banking institutions and the financial services sector. Companies can modify their services to better suit the changing demands and tastes of their clients by understanding the elements that influence customers' decisions to acquire sustainable banking services. Moreover, banks can attract and retain a growing number of socially conscious customers by aligning their services with environmental and social concerns. This contributes to the overall sustainability of the financial services sector.

The objective of this research is to examine the factors that affect the acceptance of sustainable banking services by Indonesian customers. To comprehend the reasons behind the use of sustainable banking services during interactions with financial institutions, we developed and evaluated a behavioural model to assess attitudes and intentions towards sustainable banking services.

This study aims to make a significant contribution to the literature on environmentally sustainable consumer behaviour in the banking sector. To achieve this, the Theory of Planned Behaviour (TPB) was used to investigate customer purchase intentions towards sustainable banking services. The research findings will provide valuable insights into how banks can attract customers by emphasising sustainability practices.

LITERATURE REVIEW

Sustainable Banking

Sustainable banking has evolved from its philanthropic and community development roots, known as 'social banking', to a stage where it incorporates community ethics into its business operations, known as 'ethical banking'. This has further progressed to green banking, which takes into account ecological factors. Sustainable banking involves integrating environmental, social, and governance (ESG) principles to promote sustainable development. Sustainable banking aims to promote long-term growth by funding environmentally and socially responsible enterprises. These financial institutions actively consider the long-term environmental and social consequences of their investments in addition to their financial returns [7].

Banks play an essential role in promoting sustainable development by acquiring a broad grasp of sustainability and collaborating closely with business, government, and the larger ecosystem. [8]. Green banking, corporate social responsibility, financial inclusion, and the use of sustainability reporting frameworks are all examples of sustainable banking practices in Indonesia [9,10]. The Financial Services Authority of Indonesia (OJK) released Regulation No. 51/POJK.03/2017 on sustainable finance to guide the implementation of sustainable finance. This rule mandates banks to keep and publish a sustainability report, and it applies to commercial banks BUKU 3 and 4, who were the first to implement sustainable banking practices. These regulatory actions indicate Indonesia's commitment to long-term development goals and to supporting the country's sustainable banking practices.

Theory of Planned Behaviour

The Theory of Planned Behaviour (TPB) is a socio psychological theory that explains human behaviour and decision-making. It was first proposed by Icek Ajzen in 1985 as an extension of the earlier Theory of Reasoned Action (TRA). The TRA suggests that an individual's intention to perform a behaviour is determined by their attitude towards the behaviour and subjective norms. However, the TRA did not consider circumstances that might prevent an individual from engaging in the behaviour, such as a lack of control or financial resources. To overcome this limitation, the TPB model adds a third element: perceived behavioural control. This refers to a person's confidence in their ability to act, taking into account both external and internal variables. According to the theory of planned behaviour, an individual's intention to engage in a behaviour is influenced by their attitude towards the behaviour, subjective norms, and perception of behavioural control [11].

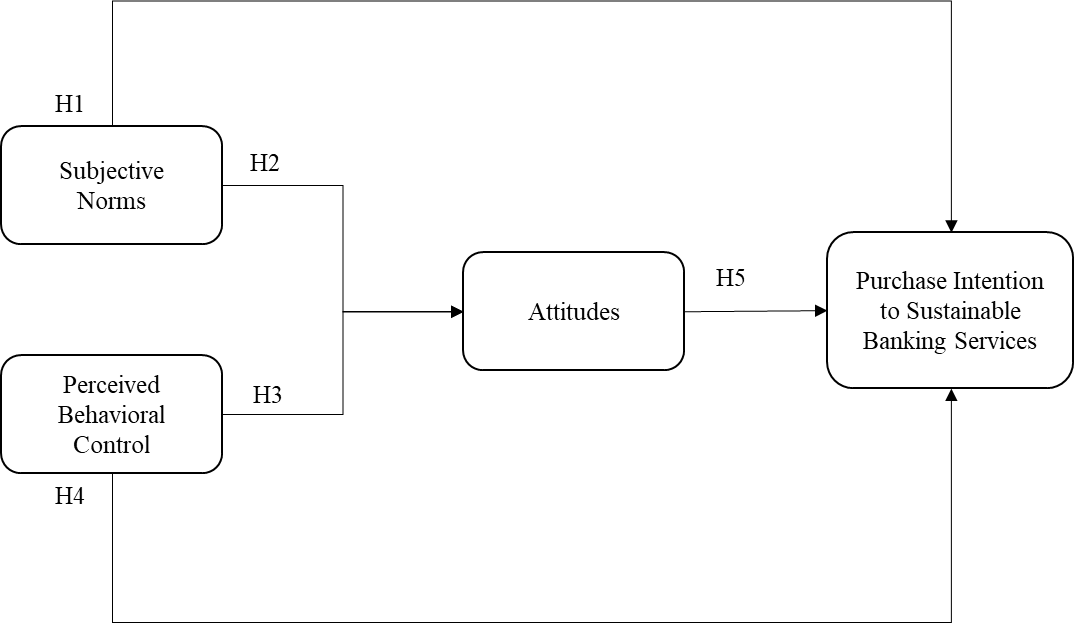

Below is conceptual framework used in this study:

The following research hypotheses were proposed:

H1: Subjective norms have a positive effect on the intention to use sustainable banking services.

H2: Subjective norms have a positive effect on attitudes toward sustainable banking services.

H3: Perceived behaviour control has a positive effect on attitudes toward sustainable banking services.

H4: Perceived behaviour control has a positive effect on intention to use sustainable banking services.

H5a: Attitude has a direct positive effect on intention to use sustainable banking services.

H5b: Attitude mediates the effect of perceived behaviour control on intention to use sustainable banking services.

H5c: Attitude mediates the effect of subjective norms on intention to use sustainable banking services.

Figure 1: Conceptual framework of sustainable banking purchase intention

Table 1: Measurement Items

List of question

Source

Subjective Norms

SN 1

People I often listen to (e.g. parents, friends, idols) will influence me to use sustainable banking services.

I plan to use financial services (e.g. saving account, time deposit, mortgages) from a sustainable banking service in the future.

PI 3

I intend to use financial services (e.g. saving account, time deposit, mortgages) from a sustainable banking service if they are available in the market.

PI 4

I would use sustainable banking services and encourage others to do the same.

MATERIALS AND METHODS

Measurements

This study employs a quantitative research methodology that focuses on the Indonesian population. The methodology was designed to collect structured and comprehensive data on customers' opinions and attitudes towards sustainability practices in the banking industry. The measurement scale was adapted from the theory of planned behaviour (TPB) [11]. A five-point Likert scale, ranging from "strongly disagree" to "strongly agree," was used to evaluate each measurement item. Bahasa Indonesia was used to translate every question on the questionnaire. Four items were used to measure purchase intention (PI1 to PI4), while attitude was measured using five items (AT1 to AT3). Three items were developed for the subjective norms’ variable (SN1 to SN3), and four items were used to measure perceived behavioural control (PBC1 to PBC4).

Sampling and Data Collection

This study uses a quantitative research methodology with a focus on the Indonesian population. The methodology used is designed to collect structured and complete data on respondents' opinions and attitudes towards sustainability practices in the banking industry. Probability sampling will be used to select respondents from the target population. Prior to administering the questionnaire to the final sample, a pretest was conducted on a group of 30 customers to verify the content validity of the scale. The data was then processed using SPSS for validity and reliability testing, which confirmed that the questionnaire passed the necessary tests. After the pre-test, we conducted the main survey by distributing online and administering questionnaires to 180 respondents.

Data Analysis

The questionnaire data were analysed using Partial Least Squares Structural Equation Modelling (PLS-SEM), a statistical approach used to examine the relationships between variables in a structural equation model [12]. The SmartPLS 3.0 software was used to conduct the statistical analysis. PLS-SEM is a statistical method used to develop a model representing hypothesised relationships between variables. Statistical analysis is then used to determine the strength and direction of these relationships.

RESULTS

Respondent Characteristics

The survey was conducted with 180 participants, of whom 107 (59,4%) were female and 73 (40.6%) were male. The majority of respondents (43,9%) were aged between 17 and 20, with 79 participants falling within this age range. 35,0% respondents were aged between 21 and 26, comprising 63 respondents and remaining 21,1% respondents were aged between 27 and 35. In terms of domicile, the majority of respondents were from Central Java (33,3%), followed by West Java (29,4%) and DKI Jakarta (23.3%). The most common educational attainment among the participants was High School (48.3%), followed by a Bachelor's degree (44,4%). The majority of the participants were students (51,1%), with a small number employed in the private sector, state-owned enterprises, or self-employed, and some were civil servants. The sample profile is summarised below.

The Measurement Model and Path Analysis

A convergent and discriminant validity analysis was performed to confirm the reliability and validity of the scale. Convergent validity was determined using factor loadings, average variance explained (AVE), Cronbach's alpha, and composite reliability. All measurement items had factor loadings greater than the recommended value of 0,7 [12], indicating indicator reliability. Cronbach's alpha was calculated to measure the internal consistency of the scale, and all constructs had values greater than 0,7. A high AVE indicates strong convergent as well as discriminant validity of the scale. Table 2 shows the results of composite reliability and Cronbach's alpha values.

Discriminant validity was determined by comparing construct correlations and the square root of their respective AVE. Results show that the square root of AVE for each construct was greater than its highest correlation with other constructs, indicating satisfactory discriminant validity. Table 3 shows a comparison of the correlations between the constructs with the square roots.

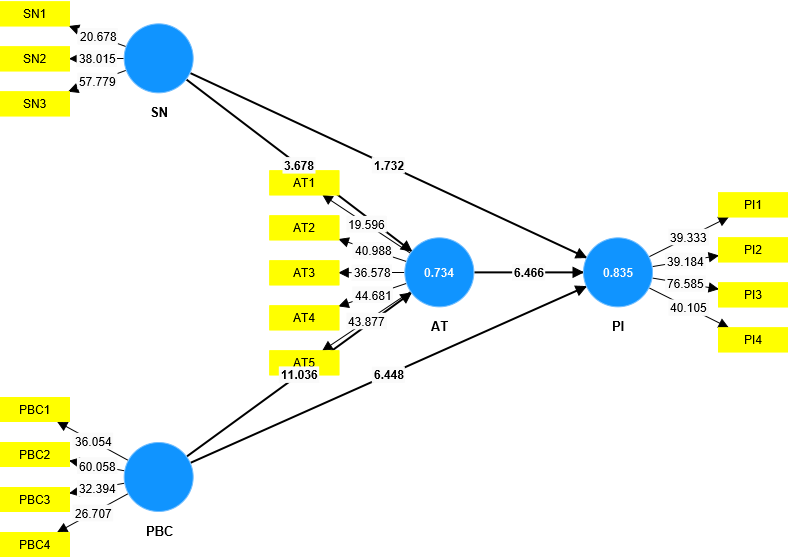

The structural model and path analysis results are presented in Table 4 and Figure 2. The coefficient of determination (R2) for the attitude variable was 0.734, and the coefficient of determination (R2) for purchase intentions was 0.835.

Based on the table provided, the R-squared value for the variable 'Attitude' is 0.734. This suggests that attitude is a significant mediating factor, influenced by subjective norms and perceived behavioural control. A high R-squared value for Attitude indicates that the combined effects of subjective norms and perceived behavioural control explain approximately 73.4% of its variance. Moreover, the R-Square value for the variable 'Purchase Intention' is 0.835, indicating that subjective norms, perceived behavioural control, and attitude have a 83.5% influence on Purchase Intention.

Hypotheses Testing

The research hypothesis is tested using p-values, t-statistics, and the path coefficient value. The p-value indicates the statistical significance of the association between the variables, while the path coefficient shows the degree of influence between them. The t-statistic assesses the significance of the relationship. The table below presents the path coefficient values, t-statistics, and p-values for the constructs.

Table 2: Convergent Validity, and Composite Reliability results

Construct

Items

Loadings

AVE

Composite reliability

Cronbach's alpha

Subjective Norms

SN 1

0,803

0,738

0,8307

0,8214

SN 2

0,879

SN 3

0,891

Perceived behaviour control

PBC 1

0,861

0,739

0,8874

0,8815

PBC 2

0,910

PBC 3

0,855

PBC 4

0,809

Attitude

AT 1

0,823

0,754

0,9210

0,9182

AT 2

0,887

AT 3

0,863

AT 4

0,883

AT 5

0,883

Purchase Intention

PI 1

0,887

0,807

0,9217

0,9203

PI 2

0,897

PI 3

0,929

PI 4

0,880

Table 3: Discriminant Validity result

AT

PBC

PI

SN

AT

0,877

PBC

0,834

0,869

PI

0,868

0,859

0,898

SN

0,687

0,644

0,678

0,859

Table 4: R-Square Value

Construct

R2 Value

Attitude

0.734

Purchase Intention

0.835

Table 5: Hypothesis Testing Results

Path Variable

Hypothesis

Path

Coefficient

T Statistics

(|O/STERR|)

P-Value

Direct Effect

Subjective Norms Purchase Intention

H1

0,086

1,732

0,083

Subjective Norms Attitude

H2

0,255

3,678

0,000

Perceived Behaviour Control Attitude

H3

0,670

11,036

0,000

Perceived Behaviour Control Purchase Intention

H4

0,431

6,448

0,000

Attitude Purchase Intention

H5a

0,459

6,466

0,000

Indirect Effect

Subjective Norms Attitude Purchase Intention

H5b

0,117

3,264

0,001

Perceived Behaviour Control Attitude Purchase Intention

H5c

0,308

5,344

0,000

Figure 2: Path Diagram Results

The results of bootstrapping the inner mode path diagram with SmartPLS 3.0 are as follows:

A 5% margin of error is used in hypothesis testing in this investigation. Thus, 1.96 is the crucial value that needs to be reached. The path coefficient value is used to determine the positive or negative effect between the exogenous and endogenous latent constructs, and the t-statistic or p-values are used to determine the significant or insignificant effect.

The data from a path analysis investigating the connection between subjective norms and purchase intention indicated a moderately strong positive association, with a path coefficient of 0.086. However, statistical significance was not established as the T-statistic value of 1.732 fell short of significance at the specified confidence level, and the P-value of 0.083, while approaching significance, did not meet the conventional threshold of 0.05. Therefore, H1 is supported by the data, indicating a potential positive impact of subjective norms on purchase intention.

Additionally, statistical analysis revealed a significant correlation between subjective norms and attitude, with a path coefficient of 0.255. To ensure the robustness of this relationship, the T T-statistic value of 3.678 and P-value of 0.000 were considered. Thus, it can be inferred that subjective norms have a significant positive impact on attitudes, resulting in the acceptance of H2. Furthermore, the data demonstrated a robust and positive correlation between perceived behavioural control and attitude (path coefficient = 0.670, T Statistics = 11.036, P-Value = 0.000), highlighting the significant role of perceived control in shaping individual attitudes. Therefore, H3 was supported.

The analysis shows a strong and statistically significant correlation between purchase intention and Perceived Behaviour Control (PBC) (path coefficient = 0.431, T statistics = 6.448, P-value = 0.000). This indicates that an individual's perceived control over their behaviour has a substantial impact on their intention to make a purchase, thus supporting H4. The data show a significant positive correlation between attitude and purchase intention. This is supported by a path coefficient of 0.459, T-statistic of 6.466, and P-value of 0.000. This finding highlights the important role of attitude in influencing consumers' purchase decisions, which supports Hypothesis H5a.

The results show a significant relationship between subjective norms and purchase intention, mediated by attitude, as indicated by a path coefficient of 0.117, a T-statistic of 3.264 and a P-value of 0.001. This suggests that subjective norms affect purchase intentions by influencing attitude, highlighting the crucial role of attitudes in shaping consumer behaviour. Therefore, hypothesis H5b is accepted. The data shows a significant association between Perceived Behaviour Control and Purchase Intention, mediated by Attitude, with a path coefficient of 0.308, T Statistics of 5.344, and a P-Value of 0.000. This indicates that an individual's perceived control over their behaviour significantly influences their intention to purchase, with this effect partially mediated through their attitude. Therefore, hypothesis H5c is accepted.

CONCLUSION

The findings suggest that Theory of Planned Behaviour can influence customer intentions to use sustainable banking services. All TPB constructs were found to significantly influence customer intention to use sustainable banking services, which in turn translated into actual behaviour.

The study found that subjective norms have a direct positive effect on attitudes and purchase intentions towards sustainable banking services. These results suggest that subjective norms play a crucial role in shaping customer attitudes and purchase intentions towards sustainable banking services. This finding is consistent with previous research that has highlighted the importance of subjective norms in shaping individuals' attitudes and behaviours towards sustainable practices [13,14].

The role of perceived behavioural control in determining purchase intention is significant. This refers to an individual's confidence in their ability to perform a desired behaviour. Research suggests that customers' perception of their ability to control their behaviour significantly influences their intention to purchase sustainable banking services. Taneja & Ali research demonstrates that perceived behavioural control positively impacts the adoption of sustainable banking services. Customers are more likely to express a positive intention to adopt sustainable banking services when they perceive control over their usage. This finding supports the applicability of the theory of planned behaviour in shaping customers' intentions towards sustainable banking services.

The results of this study indicate that attitude plays a critical role in shaping the purchase intention towards sustainable banking services. The research shows that customer’s general attitude towards sustainable banking has a direct, positive, and significant impact on their intention to make purchases of sustainable banking services. Attitude has been found to mediate the effect of subjective norms on purchase intention. Consistent with previous research, Roh et al. [15] found that subjective norms have a significant positive effect on purchase intention. The impact of subjective norms on purchase intention is influenced by customer attitudes, indicating that the formation of consumer attitudes plays a role. Social influences shape people's views when they receive feedback about the merits of particular behaviours from both internal and external sources. To promote sustainable banking services, banks should emphasise the social benefits of their services and the expectations of relevant social groups.

Moreover, the research findings indicate that attitude acts as a mediator between perceived behaviour control and purchase intention. The impact of perceived behaviour control on purchase intention is moderated by attitude, as it determines the relationship between the two variables. This finding is consistent with Yuan et al., research, which suggests that attitude mediates the relationship between perceived behavioural control and purchase intention. A positive attitude towards sustainable banking practices may strengthen the intention to adopt these practices if individuals believe they have the ability to engage in them. Those with positive attitudes are more likely to have a stronger intention to adopt sustainable banking practices, even if they perceive limited control.

REFERENCES

European Commission. (2021). Overview of Sustainable Finance. Retrieved from https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/overview-sustainable-finance_en.

Kumar, S., Sharma, D., Rao, S., Lim, W. M., & Mangla, S. K. (2022). Past, present, and future of sustainable finance: insights from big data analytics through machine learning of scholarly research. Annals of Operations Research. https://doi.org/10.1007/s10479-021-04410-8.

Migliorelli, M. (2021). What Do We Mean by Sustainable Finance? Assessing Existing Frameworks and Policy Risks. Sustainability, 13(2), 975. https://doi.org/10.3390/su13020975.

Arachchi, H. A. D. M., & Samarasinghe, G. D. (2023). Influence of corporate social responsibility and brand attitude on purchase intention. Spanish Journal of Marketing - ESIC. https://doi.org/10.1108/SJME-12-2021-0224.

Bouma, J. J., Jeucken, M., & Klinkers, L. (2017). Sustainable banking: The greening of finance. Routledge.

Becchetti, L., Bobbio, E., Prizia, F., & Semplici, L. (2022). Going Deeper into the S of ESG: A Relational Approach to the Definition of Social Responsibility. Sustainability (Switzerland), 14(15). https://doi.org/10.3390/su14159668.

Ielasi, F., Bellucci, M., Biggeri, M., & Ferrone, L. (2023). Measuring banks’ sustainability performances: The BESGI score. Environmental Impact Assessment Review, 102. https://doi.org/10.1016/j.eiar.2023.107216.

Sengupta, U., Pramanik, H. S., Datta, S., Dutta, S., Dasgupta, S., & Kirtania, M. (2023). Assessing sustainability focus across global banks. Development Engineering, 8, 100114. https://doi.org/10.1016/j.deveng.2023.100114.

Maryanti, M., Putra, F., Ariyanto, E., & Anwar, A. (2021). Banking Sustainability in Indonesia. Proceedings of the 1st International Conference on Law, Social Science, Economics, and Education, ICLSSEE 2021, March 6th 2021, Jakarta, Indonesia. https://doi.org/10.4108/eai.6-3-2021.2305976.

Saraswati, W., Sukoharsoni, E. G., Saraswati, E., & Prastiwi, A. (2022). The Effect of Sustainability Reporting Practices on The Quality of CSR Disclosures in Banking in Indonesia. International Journal of Environmental, Sustainability, and Social Science, 3(3), 644–653. https://doi.org/10.38142/ijesss.v3i3.264.

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T.

Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, Marko. (2022). A primer on partial least squares structural equation modeling (PLS-SEM).

Hasan, M. M., Al Amin, M., Moon, Z. K., & Afrin, F. (2022). Role of Environmental Sustainability, Psychological and Managerial Supports for Determining Bankers’ Green Banking Usage Behavior: An Integrated Framework. Psychology Research and Behavior Management, Volume 15, 3751–3773. https://doi.org/10.2147/PRBM.S377682.

Riza, M. F., Muhtar, M. H. I., & Alfiani, S. D. (2021). Penentu Niat Pelanggan Dan Norma Pribadi Menuju Kelestarian Lingkungan Perbankan: Menguji Model Struktural. Retrieved from https://api.semanticscholar.org/CorpusID:238675655.

Roh, T., Seok, J., & Kim, Y. (2022). Unveiling ways to reach organic purchase: Green perceived value, perceived knowledge, attitude, subjective norm, and trust. Journal of Retailing and Consumer Services, 67.https://doi.org/10.1016/j.jretconser.2022.102988

Advertisement

Recommended Articles

Research Article

Modelling Structure Job Quality, Job Design and Job Satisfaction

Moch Nurhadi,

...

Avi Sunani

Published: 30/08/2022

Download PDF

Cite

x

APA

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. & Sunani, A. (2022). Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management, 3(2), 1-4.

MLA

Nurhadi, Moch, et al. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3.2 (2022): 1-4.

Chicago

Nurhadi, Moch, Moch Bisyri Effendi, Achmad Saiful Ulum and Avi Sunani. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3, no. 2 (2022): 1-4.

Harvard

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. and Sunani, A. (2022) 'Modelling Structure Job Quality, Job Design and Job Satisfaction' Himalayan Journal of Economics and Business Management 3(2), pp. 1-4.

Vancouver

Nurhadi M, Bisyri Effendi M, Saiful Ulum A, Sunani A. Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management. 2022 Jul;3(2):1-4.

Download PDF

Research Article

Accountability and Transparency of Village Fund Management in Lumajang District

Nurina Ayuningtiyas,

...

Muhammad Miqdad

Published: 28/12/2023

Download PDF

Cite

x

APA

Ayuningtiyas, N., Santosa Putra, H. & Miqdad, M. (2023). Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management, 4(2), 1-4.

MLA

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4.2 (2023): 1-4.

Chicago

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4, no. 2 (2023): 1-4.

Harvard

Ayuningtiyas, N., Santosa Putra, H. and Miqdad, M. (2023) 'Accountability and Transparency of Village Fund Management in Lumajang District' Himalayan Journal of Economics and Business Management 4(2), pp. 1-4.

Vancouver

Ayuningtiyas N, Santosa Putra H, Miqdad M. Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management. 2023 Jul;4(2):1-4.

Download PDF

Research Article

Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya

Kinisu Sifuna,

...

Peter Simotwo

Published: 30/06/2021

Download PDF

Cite

x

APA

Sifuna, K., Lwangale, D. W., Simotwo, P., Sifuna, K., Lwangale, D. W. & Simotwo, P. (2021). Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya. Himalayan Journal of Economics and Business Management, 2(1), None-None.

MLA

Sifuna, Kinisu, et al. "Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya." Himalayan Journal of Economics and Business Management 2.1 (2021): None-None.

Chicago

Sifuna, Kinisu, David W. Lwangale, Peter Simotwo, Kinisu Sifuna, David W. Lwangale and Peter Simotwo. "Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya." Himalayan Journal of Economics and Business Management 2, no. 1 (2021): None-None.

Harvard

Sifuna, K., Lwangale, D. W., Simotwo, P., Sifuna, K., Lwangale, D. W. and Simotwo, P. (2021) 'Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya' Himalayan Journal of Economics and Business Management 2(1), pp. None-None.

Vancouver

Sifuna K, Lwangale DW, Simotwo P, Sifuna K, Lwangale DW, Simotwo P. Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya. Himalayan Journal of Economics and Business Management. 2021 Jan;2(1):None-None.

Download PDF

Research Article

The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022

Fathurrozi Azhar Edyansyah,

...

Agung Budi Sulistiyo

Published: 05/07/2025

Download PDF

Cite

x

APA

Azhar Edyansyah, F., Prasetyo, W. & Budi Sulistiyo, A. (2025). The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022. Himalayan Journal of Economics and Business Management, 6(2), 1-4.

MLA

Azhar Edyansyah, Fathurrozi, Whedy Prasetyo and Agung Budi Sulistiyo. "The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022." Himalayan Journal of Economics and Business Management 6.2 (2025): 1-4.

Chicago

Azhar Edyansyah, Fathurrozi, Whedy Prasetyo and Agung Budi Sulistiyo. "The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022." Himalayan Journal of Economics and Business Management 6, no. 2 (2025): 1-4.

Harvard

Azhar Edyansyah, F., Prasetyo, W. and Budi Sulistiyo, A. (2025) 'The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022' Himalayan Journal of Economics and Business Management 6(2), pp. 1-4.

Vancouver

Azhar Edyansyah F, Prasetyo W, Budi Sulistiyo A. The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022. Himalayan Journal of Economics and Business Management. 2025 Jul;6(2):1-4.

Radifan, J., Sufiati, M. & Hamsal, M. (2024). The Roles of Attitude, Subjective Norm, And Perceived Behavioural Control in Determining Consumers' Behavioural Intentions Towards Sustainable Banking Services. Himalayan Journal of Economics and Business Management, 5(1), 1-6.

MLA

Radifan, Jamal, Mustika Sufiati and Mohammad Hamsal. "The Roles of Attitude, Subjective Norm, And Perceived Behavioural Control in Determining Consumers' Behavioural Intentions Towards Sustainable Banking Services." Himalayan Journal of Economics and Business Management 5.1 (2024): 1-6.

Chicago

Radifan, Jamal, Mustika Sufiati and Mohammad Hamsal. "The Roles of Attitude, Subjective Norm, And Perceived Behavioural Control in Determining Consumers' Behavioural Intentions Towards Sustainable Banking Services." Himalayan Journal of Economics and Business Management 5, no. 1 (2024): 1-6.

Harvard

Radifan, J., Sufiati, M. and Hamsal, M. (2024) 'The Roles of Attitude, Subjective Norm, And Perceived Behavioural Control in Determining Consumers' Behavioural Intentions Towards Sustainable Banking Services' Himalayan Journal of Economics and Business Management 5(1), pp. 1-6.

Vancouver

Radifan J, Sufiati M, Hamsal M. The Roles of Attitude, Subjective Norm, And Perceived Behavioural Control in Determining Consumers' Behavioural Intentions Towards Sustainable Banking Services. Himalayan Journal of Economics and Business Management. 2024 Jan;5(1):1-6.