Over the years, the issues of exchange rate volatility and macroeconomic performance has continued to occupy the front banner in macroeconomic researches all over the world. Different methods have been employed by various researchers and scholars both in developed and developing economies to unravel the impact of exchange rate volatility on output growth such as [1,2]. In Africa, several measures have been taken by various governments in some ECOWAS member countries in order to ensure increase in output of goods and services; one of such measures is to adopt a floating exchange rate thereby devalue their currency. The aim of this is to make their products cheaper at international market and promote output growth. However, after some of the ECOWAS countries adopted floating exchange rate regime, the nominal exchange rate became more volatile [3].

With the introduction of this form of modern trade and the modernization of the production sector most developing countries have very low comparative advantages to that of developed nations that have the balanced growth path and still at continue on the balanced growth path, they are highly at advantage them poorer countries that are considered partners in trade. In order words, poorer countries highly depend on richer countries for the major transaction of key commodities to the economies, which the West African countries are of no exception [3]. The exchange rate is among those macroeconomics indicators that have a significant effect on the scope of other macroeconomic aggregates and most importantly it has a great impact on the Gross Domestic Product (GDP), money supply, interest rate and inflation rate. However, the impact of exchange rate on economic growth and the determination of economic performance is key among scholars, academicians and policymaker which most of them pointing at exchange rate excitability as relevant attribute to the financial crisis in the world economic performance and most of all the unpredictable increasing inflation in West African countries, the study of exchange rate has been a point of controversy considering it contribution on the determination of macroeconomic performance, exchange rate has experienced huge both empirical and theoretical studies. From the standpoint of microeconomic, figure out that exchange rate excitability decreases the macroeconomic performance which leads to a huge reduction in savings or Gross Domestic Product as raises the cost of international trade as well as the increasing of capital flows which hampering investment activities and causing macroeconomic instability for the Economic Community of West African States (ECOWAS) member countries namely, Niger, Mali, Mauritania, Burkina Faso, Senegal and The Gambia others include, Guinea-Bissau, Guinea, Sierra Leone, Liberia, Ivory Coast, Ghana, Togo, Benin and Nigeria.

Statement of the Problem

The persistent fluctuations of the exchange rate have dominated recent literature in international finance owing to its effects on developing economies. Since the embracing of financial liberalization strategies, most developing countries have been exposed to sharp exchange rate fluctuations. Volatile exchange rates are related to unplanned fluctuations of relative prices in the economy. Therefore, exchange rate stability is among the major factors affecting stable economic growth, price stability and foreign (direct and portfolio) investments [5].

However, some studies have discovered the presence of negative effects of exchange rate volatility on some macroeconomic indicators that may affect economic growth such as GDP, employment, investment, international trade and inflation [6]. Furthermore, it was identify it was lack of continuity and inconsistency in policies on exchange rate policies combined with the unstable price of primary produces of ECOWAS member countries that result exchange rate fluctuation [7]. According to Omojimite and Akpokodje [8], exchange rate volatility has been affected by structural shifts in production, institutional changes in the economy and the changing pattern of international trade. Countries have applied monetary policies that maintain exchange rates by adopting either fixed or flexible exchange rate regimes. Therefore, it is in the light of these backdrops that this study examines the impact of exchange rate volatility on economic growth in ECOWAS countries.

Objectives of the Study

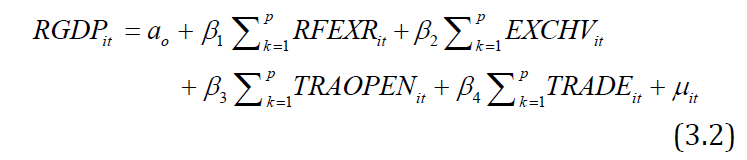

The aim of the study is to examine the impact of exchange rate volatility on economic growth in ECOWAS countries. The specific objectives are to:

Conceptual Literature

Exchange Rate Volatility: A foreign exchange rate is the price of the domestic currency stated in terms of another currency. In other words, a foreign exchange rate compares one currency with another to show their relative values. Since standardized currencies around the world float in value with demand, supply and consumer confidence, their values change relative to each over time. For instance, one US dollar in 2011 was worth about .68 Euros. In 2014, one US dollar is worth 0.75 Euros. This means the dollar has increased in value over this three-year span, but the Euro is still 25% more valuable [13].

An exchange rate is the value of one nation's currency versus the currency of another nation or economic zone. For example, how many U.S. dollars does it take to buy one euro? As of September 24, 2021, the exchange rate is 1.1720, meaning it takes $1.1720 to buy €1 [10].

Economic Growth

Economic growth is the increase in the value of goods and services produced by a country over a period and Real Gross Domestic Product (RGDP) is used as a proxy for economic growth. Real gross domestic product is an inflation-adjusted measure which reflects the value of all goods and services produced by an economy in a given year, usually expressed in base-year prices and is often graded as constant-price or inflation-corrected GDP. Unlike nominal GDP, real GDP can account for changes in price level and provide a more accurate figure of economic growth [11]. According to Salami et al. [12], economic growth can be defined as the sustained increase in a country’s productive capacity and per capita national output or net national product over a while. These increases are the basic causes of economic growth. Fiscal policy is one of the most important tools that have a significant effect on all economic sectors and have a real effect on economic variables like the Gross national product, inflation, unemployment, etc. Taxes can be seen as a fiscal policy, macroeconomic and internal revenue mobilization tool for the attainment of economic growth. Economic growth can be proxied, using different economic indicators, ranging from Gross National Product (GNP), Gross Domestic Product (GDP), Human Development Index and Per Capita Income. But in this study, economic growth was measured with Gross Domestic Product (GDP) and Human Development Index.

Theoretical Literature

Purchasing Power Parity Theory: The purchasing power parity theory was propounded by Professor Gustav Cassel of Sweden in 1932. According to this theory, rate of exchange between two countries depends upon the relative purchasing power of their respective currencies. Such will be the rate which equates the two purchasing powers. For example, if a certain assortment of goods can be had for £1 in Britain and a similar assortment with Rs. 80 in India, then it is clear that the purchasing power of £ 1 in Britain is equal to the purchasing power of Rs. 80 in India. Thus, the rate of exchange, according to purchasing power parity theory, will be £1 = Rs. 80.

Let us take another example. Suppose in the USA one $ purchases a given collection of commodities. In India, same collection of goods cost 60 rupees. Then rate of exchange will tend to be $ 1 = 60 rupees. Now, suppose the price levels in the two countries remain the same but somehow exchange rate moves to $1=61 rupees. This means that one US$ can purchase commodities worth more than 46 rupees. It will pay people to convert dollars into rupees at this rate, ($1 = Rs. 61), purchase the given collection of commodities in India for 60 rupees and sell them in U.S.A. for one dollar again, making a profit of 1 rupee per dollar worth of transactions.

This will create a large demand for rupees in the USA while supply thereof will be less because very few people would export commodities from USA to India. The value of the rupee in terms of the dollar will move up until it will reach $1 = 60 rupees. At that point, imports from India will not give abnormal profits. $ 1 = 60 rupees and is called the purchasing power parity between the two countries.

Interest Rate Parity Theory

It was developed by Keynes in 1930 and applies the law of one price. Interest Rate Parity (IRP) is a theory in which the differential between the interest rates of two countries remains equal to the differential calculated by using the forward exchange rate and the spot exchange rate techniques. Interest rate parity connects interest, spot exchange and foreign exchange rates. It plays a crucial role in Forex markets. IRP theory comes handy in analyzing the relationship between the spot rate and a relevant forward (future) rate of currencies. According to this theory, there will be no arbitrage in interest rate differentials between two different currencies and the differential will be reflected in the discount or premium for the forward exchange rate on the foreign exchange. The theory also stresses on the fact that the size of the forward premium or discount on a foreign currency is equal to the difference between the spot and forward interest rates of the countries in comparison.

Empirical Literature

The link between exchange rate volatility and economic growth has attracted the attention of the researchers and scholars. The empirical review of literature was written as follows.

Pabai [13] examined the effects of exchange rate volatility on economic growth in four WAMZ countries. The study uses the pooled ordinary least squares, fixed effects and random effects models and obtains a robust standard error estimate of the model by applying xtreg, cluster. The empirical analysis shows that the effect of exchange rate volatility on economic growth is insignificant. Also, the results show a positive correlation between exports and economic growth. This fact implies that policies aimed at increasing exports through an appropriate exchange rate may be beneficial to the countries. In addition, the analysis also shows a positive and significant link between imports and growth rates. Therefore, this confirms that the countries actually benefit from imports resulting from the competitive pressure generated by the import of consumer goods and professional knowledge and also from the transfer of technology embodied in the import of goods by producers. Hence, the policy of removing import barriers will benefit the countries. Furthermore, the results show that there is a positive correlation between the nominal exchange rate and economic growth rate. Thus, this shows that the nominal exchange rate depreciation policy can play an important role in improving the growth of the countries. However, the research results show that there is an inverse relationship between the real exchange rate and growth. Considering the importance of the real exchange rate, this finding suggests the introduction of a common currency in the WAMZ economies to reduce the negative effects on growth. Prudent exchange rate via monetary policy can be developed and implemented to promote growth.

Phebe-Padolo [4], conducted a study to examine impact of exchange rate volatility on economic growth in ECOWAS member countries. This study applied the Dynamic Ordinary Least Squares (DOLS) technique to the panel data from the year 2000 to 2018 to prove empirical evidence on the long-run relationship between exchange rate and economic growth in the Economic Community of West Africa States (ECOWAS) member countries. The study generated the annual data from World Development Indicators (WDI) of the World Bank, data of the fifteen member countries. Data collected for those variables were analyzed using the econometrics technique of the panel fixed-effect model. The paper found a negative relationship between exchange rate and economic growth at 0.006 and statistically significant at both 5 and 10% percentages level of significant, the results show negative impact of real interest rate on economic growth at 0.20 and statistically significant at both 5 and 10% (percentages) level of significance in the ECOWAS member countries. The results also show the existence of positive relationships among labor and per capita income on economic growth (GDP) to be 0.24 and 0.41 significant at both 5 and 10% (percentages) level respectively in ECOWAS member countries. The granger causality test results have shown the relationship to be unidirectional causality from economic growth to the exchange rate. This investigation concluded that the exchange rate is a significant factor for policymakers to consider in process of monetary policy formulation in the stimulation of economic growth in ECOWAS member countries.

Ariyo and Olalere [14] examined the impact of exchange rate volatility on output growth in the ECOWAS, using time series data spanning from 1980 to 2015. The study employed panel data analysis to examine the relationship between exchange rate volatility and output growth among the selected countries within the ECOWAS countries. GARCH was used to establish the existence of volatility while Panel ARDL was used to assess the magnitude of the effects of exchange rate volatility on output growth in ECOWAS. The result of volatility test from GARCH confirmed the presence of volatility in Real Effective Exchange Rate (REER) across all the selected countries in ECOWAS. Furthermore, the short run ADRL results revealed that, there is a negative but insignificant relationship between exchange rate volatility and output growth in ECOWAS while the long-run ARDL results showed that, exchange rate volatility has positive but insignificant impact on output growth in ECOWAS. Based on the findings of this study, it is therefore recommended that exchange rate policy that will pave way for competitiveness should be formulated by monetary authorities in ECOWSA. In addition, ECOWAS countries should endeavour to add more value to their products before exporting them to other countries.

Umaru et al. [15] conducted a study to examine the effects of exchange rate volatility on economic growth of West African English speaking countries. Macroeconomic data used for this study were obtained from World Bank Data Stream between 1980 until 2017 and analyzed using Stata 14 panel data regression analysis. The results obtained showed that the independent variable (real exchange rate) is statistically significant and negatively related to the dependent variable (GDP) in West African English speaking countries excluding time-invariant variables. This current study contributes empirically regarding the relationships between exchange rate volatility and economic growth of West African English speaking countries. The recommended that findings of this study will help the countries under review and other nations in general to improve on monetary policy; it could be used by the central bank of West African English speaking countries as a guide for effective monetary policy.

Idris et al. [16] conducted a study to investigate effect of exchange rate volatility on the output level of the five English speaking countries in ECOWAS, namely Nigeria, Ghana, Gambia, the Sierra Leones and Liberia, over the period 1991 to 2014. Co-integration test and error correction modelling were used as estimation techniques. Estimates of co-integration relations were obtained and the short-run and long-run dynamic relationships between the variables were obtained for each country utilizing the tests. In general, exchange rate volatility has a significant impact on outputs at least for all the countries considered in the study, with all except Liberia having negative impact.

Gap in Literature

After literature review, it was verified that there are limited studies on impact of exchange rate volatility on economic growth in ECOWAS countries covering 20 years across 4 selected countries covering from 2001 to 2021. Scholars have paid less attention on area of the research interest taking cognizant cross sectional econometrics study and made use up to eighty number of observations

After literature review, it is verify that there is no clear consensus till date in the literature as to whether exchange rate volatility stimulate economic growth or retard economic growth as empirical result varies from region to region and country to country. The study will provide explanation to the direction effect of exchange rate volatility on economic growth thereby bridge existing gap.