This research belongs to the type of explanatory research. The purpose of this study is to determine the pattern of the relationship between profitability, capital structure and firm value in real estate and property sector companies. The sample in this study are real estate and property companies listed on the Indonesia Stock Exchange. the period 2016 - 2019. The data used in this study were obtained through www.idx.co.id and the websites of each real estate and property company listed on the IDX for the period 2016 - 2019. The sampling technique in this study used the purposive sampling method, namely the determination of the sample based on criteria including real estate and property companies listed on the Indonesia Stock Exchange for the 2016-2019 period, not having negative equity and profits. The data analysis technique used in this study used the SEM-PLS method with SMART-PLS software. The results showed that NPM and ROA were able to measure profitability. DAR and DER are able to measure capital structure. PER and PBV are able to measure firm value. The results showed that all hypotheses were accepted, which means that profitability has a significant positive effect on firm value, profitability has a significant positive effect on capital structure, capital structure has a significant positive effect on firm value, capital structure can partially mediate the effect of profitability on firm value. Mediation test shows that capital structure is a mediating variable between profitability and firm value. Companies must be able to increase profitability so as to improve the capital structure which will increase the value of the company. Further research can discuss and discuss research on capital structure on firm value with various different indicators such as dividend yield, dividend payout ratio, and other indicators for the company's financial performance variables as well as increasing the research period so as to produce more representative results.

Keywords

Capital Structure

Firm Value

Probability

SEM-PLS

INTRODUCTION

Optimization of Firm Value is the company's main goal, therefore every company must always maintain and improve Firm Value in order to survive, be sustainable and be able to compete with other companies [1]. According to Noerirawan [2], a Firm Value is a picture of public trust in the company which is also a condition of the achievements of a company since the company was founded until now. Soliha et al. [3] state that if a company shows a high share price, it will have an impact on increasing Firm Value. A high Firm Value can show that the prosperity of shareholders also increases. Alfredo [4] explain that the establishment of a company's short-term goal is to achieve maximum profit. The company's long-term goal is to prosper its shareholders or investors.

One of the factors that can affect Firm Value is Profitability. The purpose of the company or business is to create profits, the profits obtained can be used as a benchmark for the welfare of its investors. Profitability is the company's ability to generate profits. The profit can be linked through sales, total assets and own capital used in the company's operational activities. The size of the total assets, sales and capital may not necessarily generate large profits. Riyanto [5] argues that most companies are more concerned with profitability than profit, because high profits cannot be used as a benchmark that companies run their operations efficiently. Efficiency can be seen through the comparison between the profits obtained by the company compared to the capital that generates profits, therefore profitability can be used as a measure of efficiency. A company that has high profitability will bring a positive signal for investors to invest their funds in the company. The increasing interest of these investors can affect the increase in the company's stock price so that it will have an impact on increasing Firm Value. These results are in accordance with the results of research conducted by [6].

On the other hand, profitability can also affect Firm Value through capital structure. The greater the value of a company's profitability, the larger the portion of debt in the company's capital structure to finance operational activities will decrease. Capital structure can also affect Firm Value, if the more debt carried out by the company exceeds the optimal limit, it will increase the risk of bankruptcy and in the end investors will avoid companies with capital structures that have a large portion, due to the risk of bankruptcy. However, on the other hand, debt can serve as an incentive for the company to generate profits, assuming the company carries out its operational activities efficiently. So that the greater the debt carried out by the company is still at the optimal point, it can generate profits. This is a positive signal for investors to invest in the company, it will have an impact on increasing the value of the company. Research conducted by [7,8,9] found that capital structure significantly mediates the effect of profitability on Firm Value. However, the opposite is proven by Thaib [10] that capital structure does not mediate the effect of profitability on Firm Value.

The object of this research is real estate and property companies that go public on the Indonesia Stock Exchange. The selection of the sample is based on the main problems faced by real estate and property companies that go public on the IDX. The problem is the increasing amount of debt owned by real estate and property companies that went public on the Indonesia Stock Exchange starting from 2015 to 2018. If the real estate and property companies continue, it can have an impact on the survival of the company. The high level of debt will have an impact on decreasing the interest of investors to invest in the company. This study was conducted to determine the relationship pattern between Capital Structure, Profitability and Firm Value of real estate and property listed on the Indonesia Stock Exchange for the 2016-2019 period.

Literature Review

Trade Off Theory: Trade-off theory states that the decision of each company to use debt is based on a balance between the benefits of debt, namely tax savings and debt costs or financial difficulties [11]. The optimal level of debt is reached when the tax savings equal the marginal cost of debt or the cost of financing through debt. This theory assumes that there are tax benefits due to the use of debt, so companies will use debt to a certain level to maximize profits. So, based on this theory, the company tries to maintain the targeted capital structure as long as it provides benefits with the aim of getting maximum profit.

Signaling Theory

Modigliani and Miller state that managers and investors have the same information about the company's prospects or symmetrical information [12]. In fact, managers have more information than outside investors. Signal theory explains how companies should be able to provide signals to users of financial statements, especially investors who will invest.

Packing Order Theory

This theory argues that when a company needs funds for investment needs, the company uses an internal source of funds, namely retained earnings, if internal funds are insufficient, it can borrow funds or issue new shares to meet investment needs [13]. This packing order theory explains that companies that have high profits are companies that use smaller debt. This is due to the low level of debt, not because the company has a low target debt level, but because the company does not need a lot of external funds.

Capital Structure

According to Martono [14] in capital structure theory it is assumed that changes in capital structure originate from the issuance of bonds and the repurchase of ordinary shares or issuance of new shares. Furthermore, it is necessary to study how the influence of the capital structure on the value of the company and whether there is an influence of capital structure on the company's stock price as a reflection of the company's value. If there is an effect of capital structure on firm value, the next question is how the optimal capital structure for the company. In this capital structure analysis several assumptions are used, namely: 1. No income tax 2. No profit growth 3. Payment of all profits to shareholders in the form of dividends 4. Changes in capital structure occur by issuing bonds and repurchasing ordinary shares or by issue ordinary shares and withdraw bonds. According to Sartono [15] there are 2 approaches that can be used, namely as follows:

Net operating income approach (Net Operating Income Approach) Net operating income approach was proposed by David Durand in 1952. This approach assumes that investors have different reactions to the use of corporate debt. This approach sees that the weighted average cost of capital is constant regardless of the level of debt used by the company. Thus, first, it is assumed that the cost of debt is constant. Second, the increasing use of debt by the owners of their own capital is seen as an increase in company risk

Traditional Approach (Traditional Approach) In the traditional approach it is assumed that there is a change in optimal capital structure and an increase in the total value of the company through the use of financial leverage

Profitability

According to Scott and Brigham [16] Profitability can be defined as the company's ability to generate profits (profit). Profit is often a measure of the performance of a profit-oriented company. The short-term goal of a company is to make a profit, so profitability is one of the concerns for analysts and investors. The level of profitability that consistently grows will be able to stay in business by obtaining adequate returns compared to the risks [17]. According to Saidi [18] profitability is the company's ability to earn profits. Investors invest in a company with the aim of getting a return, which returns consist of dividend yields and capital gains. The higher the ability to earn profits, the greater the return expected by investors, thus making the value of the company higher.

Companies that have high profits mean good performance. Performance appraisal can be seen from the profitability ratio. Profitability ratio is a ratio that measures the company's ability to generate profits by using the sources owned by the company, such as assets, capital, or company sales [11].

According to Devi and Haryanto [19] Profitability is the company's ability to earn a profit or profit. Profitability shows the success of a business entity in generating returns. In addition, profitability is very important for companies to measure the company's ability to generate profits and as a measuring tool for management performance. Profitability is used to measure the effectiveness of overall management which is indicated by the size of the level of profit obtained. The better the profitability, the better it describes the company's high profitability [20].

Firm Value

Firm Value is created by the company through company activities in order to achieve a maximum Firm Value above the book value of Zuhroh [21]. Assessment of a company in the field of accounting and finance is still diverse. On the one hand, the value of the company is shown by the company's financial statements, especially the statement of financial position which contains past financial information, while on the other side, the firm value is reflected in the value of the company's shares. Based on investor perception Firm Value is often associated with stock prices. A company that has a high share price can have an impact on the high value of the company.

Myers [22] proposed the concept of Firm Value as a combination of assets owned and investment options in the future. Zuhroh [21], states that Firm Value can be interpreted as the company's selling value and added value for shareholders. Firm Value as the present value of the company's expected cash flows, or the future Firm Value discounted at the cost of capital level. According to Weston and Thomas [23] maximizing value means considering the effect of time on the value of money, funds received this year are worth more than funds received in the coming year and also means considering various risks to income streams. Alfredo [4], explains that firm value is an important concept for investors, because it is an indicator for the market in assessing the company as a whole. Horne [24] states that Firm Value is the price that prospective buyers are willing to pay if the company is sold.

Tandelilin [25] The high stock price makes the firm value also high. A high firm value will make the market believe not only in the company's current performance but also in the company's prospects in the future. Firm value is often proxied by price to book value and price earning ratio. Price to book value can be interpreted as the result of a comparison between stock price and book value per share [26]. Maximizing Firm Value is very important for a company because maximizing Firm Value means maximizing the company's main goal. The increase in Firm Value is an achievement that is in accordance with the wishes of the owners, because with the increase in Firm Value, the welfare of the owners will also increase.

Besley et al. [16], Firm Value is the selling value of a company as an operating business. The existence of excess selling value above the value of liquidity is the value of the management organization that runs the company. Firm value is the present value of free cash flow in the future at a discount rate according to the weighted average cost of capital [27]. Free cash flow is cash flow available to investors (creditors and owners) after taking into account all expenses for company operations and expenditures for investment and net current assets [28,29].

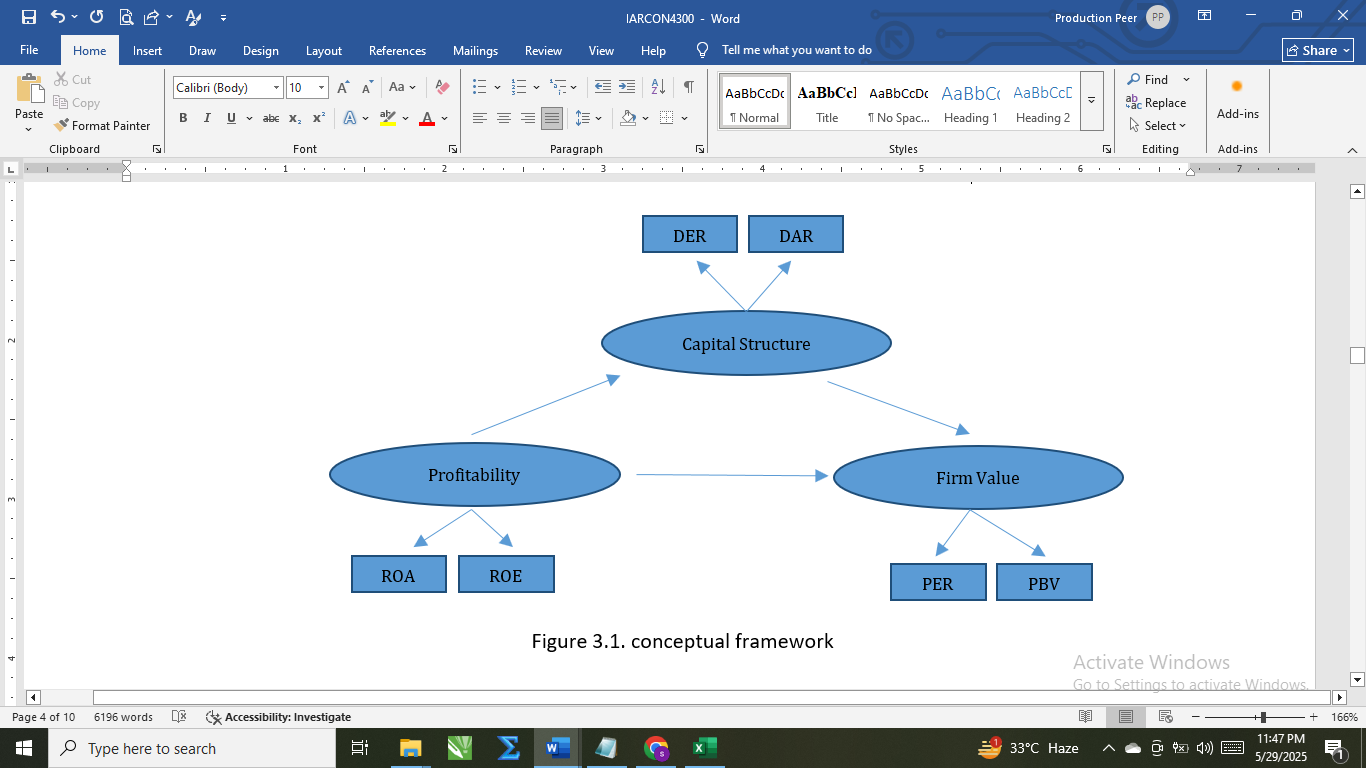

Conceptual Framework

Based on the background of the problem, the formulation of the problem, the research objectives achieved and the theory used in this study, the conceptual framework of this study is presented in Figure 1 as follows.

Figure 1: Conceptual framework

MATERIALS AND METHODS

Research Method

This research includes explanatory research. Explanative research or explanatory research (explanative research) aims to explain what happens if certain variables are controlled and manipulated in a certain way [30]. Sources of data used in this study using secondary data. Secondary data in this study were obtained through www.idx.co.id and through the websites of each company. This study aims to determine the pattern of the relationship between profitability, capital structure and Fiem Value in real estate and property sector companies. The population in this study uses real estate and property companies listed on the Indonesia Stock Exchange for the 2016-2019 period. In this study, the sampling technique used purposive sampling, in which the determination of the research was based on predetermined criteria. The criteria for this research include:

Real Estate and Property Companies listed on the Indonesia Stock Exchange during the 2016-2019 period

Real Estate and Property Companies that publish their financial reports for the period 2016-2019

Real Estate and Property Companies that do not have negative equity

Companies that do not have negative profits

There are 3 variables used in this study, namely endogenous variables using Firm Value with indicators (PER and PBV), Exogenous variables in this study using Profitability with indicators (ROA and NPM), while Intervening Variables in this study used Capital Structure with indicators (DAR and DER). The data analysis technique in this study used SEM-PLS with the help of SMART-PLS 2.0. There are two stages of using SEM-PLS, namely where the analysis in SEM-PLS consists of 2 stages, namely the outer model test related to the validity and reliability of the latent variable, while the inner model test is to test the relationship between latent variables and test hypotheses.

RESULTS

Data analysis performed in this research is Structural Equation Model-Partial Least Square analysis which consists of outer models and inner models. Where the outer model to see the validity and reliability of indicators of latent variables while the inner model to see the relationship between latent variables and test the research hypothesis. The analysis will be described as follows.

Outer Model

In the SEM-PLS outer model is divided into 2, namely, indicators that are reflective, measurements using the Confirmatory Factor Analysis (CFA) method and formative indicators, the measurement uses Explanatory Factor Analysis (EFA). In this study the indicators used are reflective, so to measure the validity and reliability using the Confirmatory Factor Analysis (CFA) method [31]. There are three criteria measuring outer models using the Confirmatory Factor Analysis (CFA) method, namely, Convergent Validity, Discriminant Validity and Composite Reliability. In this research, SEM-PLS processing uses the help of SMART-PLS 2.0 software. The measurement of Confirmatory Factor Analysis (CFA) on Smart- PLS 2.0 on PLS - Alogrithm results in a structural model presented in Figure 2 as follows.

Based on Figure 2, the results of SEM-PLS processing with Smart-PLS 2.0 software, an outer model analysis can be performed using the Confirmatory Factor Analysis (CFA) method which is divided into three stages as follows.

Figure 2: Structural Equation

Source: Data processed with Smart-PLS 2.0

Covergen Validity

The initial measurement of Confirmatory Factor Analysis (CFA) is done by looking at convergent validity which consists of 3 stages: Looking at the loading factor of each indicator measuring the latent variables namely PBV and PER measuring the value of the company, DER and DAR measuring capital structure, ROA and NPM measuring profitability. Where a loading factor fulfills convergent validity criteria if the value is more than 0.7 with the Average Variance Extracted (AVE) value and the communality value is more than 0.5. The value of the lodging factors of each indicator for the latent variable from the results of processing with Smart-PLS 2.0 software can be seen in Table 1.

Table 1 informs that the loading value of the PBV and PER factors measuring cFirm Values is more than 0.7, in accordance with convergent validity criteria. The loading value of the NPM and ROA factors that measure profitability is more than 0.7, according to the convergent validity criteria. The loading value of DER and DAR factors that measure capital structure is more than 0.7 according to convergent validity criteria. Other measures that must be met to measure convergent validity are the average Variance Extracted Value (AVE) and the communality value of more than 0.5.

Table 2 informs that the Average Variance Extracted (AVE) and communality values of all latent variables (firm value, profitability, capital structure) are more than 0.5, according to convergent validity criteria. Based on the results of Table 1 and 2, it can be concluded that each indicator of its latent variable meets the convergence validity criteria, namely loading factors of each indicator to its latent variable more than 0.7 and the Average Variance Extracted (AVE) and communality of each of its latent variables more than 0.5.

Discriminant Validity

Discriminant validity is carried out to ascertain the extent to which a construct is truly different from another construct by empirical standards. A good model if the discriminant validity for each loading value on the indicator of a latent variable has the largest value with other loading values. In this study, the results of discriminant validity processing using Smart-PLS 2.0 are listed in Table 3.

Table 3 informs that the factor loading value of each indicator that measures its latent variables (PBV and PER measures the value of the company, NPM and ROA measures profitability, DER and DAR measure capital structure) is greater than the factor loading value of the other variables/variables not measured, in accordance with cross laoding criteria on discriminat validity measurements. Furthermore discriminat validity can be seen by comparing the AVE roots with correlation values between latent variables. If the root value of AVE is greater than the correlation value, it can be said that dicriminat vaidity is fulfilled. The correlation values of the processing with Smart-PLS 2.0 software are as follows.

Table 1: Loading Factors

Firm Value

Profitability

Capital Structure

PBV

0,9298

PER

0,7559

NPM

0,8081

ROA

0,9795

DER

0,9388

DAR

0,9782

Source: Data is processed with Smart-PLS 2.0

Table 2: Average Variance Extracted (AVE) and Communality values

AVE

Communality

Firm Value

0,7179

0,7179

Profitability

0,8062

0,8062

Capital Structure

0,9192

0,9192

Source: Data is processed with Smart-PLS 2.0

Table 3: Nilai Cross Loading

Indicator

Firm Value

Profitability

Capital Structure

PBV

0,9298

0,4723

0,4343

PER

0,7559

0,2049

0,3021

NPM

0,1973

0,8081

0,0347

ROA

0,4771

0,9795

0,2852

DER

0,2947

0,1798

0,9388

DAR

0,5109

0,2569

0,9782

Source: Data is processed with Smart-PLS 2.0

Tabel 4: Laten Correlation

Firm Value

Profitability

Capital Structure

AVE Root

Firm Value

1

0,847

Profitability

0,433

1

0,897

Capital Structure

0,445

0,236

1.

0,958

Source: Data is processed with Smart-PLS 2.0

Table 4 informs that the AVE roots are greater than the late correlation, according to the criteria of discriminat validity. Based on Tables 3 and 4, it can be concluded that each indicator of the latent variable meets the criteria of discriminat validity. Based on the results of convergent validity and discriminat validity processing in Tables 1-4, it can be concluded that each indicator is valid which means it is able to measure well its latent variables.

Reliability Validity

Reliability validity in research is an index that shows the extent to which an indicator can be trusted or reliable. If an indicator is used twice or more to measure the same symptoms and the measurement results obtained are relatively consistent, then the indicator is reliable. In other words, reliability indicates the consistency of an indicator within the same symptom measure. In this study the reliability reliability uses the method of composite reliability and Cronbachs alpha, an indicator is said to meet reliability validity if the composite validity and cronbachs alpha values are more than 0.6. The results of reliability validity using Smart-PLS 2.0 software are provided in Table 5.

Table 5 informs that all the composite reliability values and Cronbach's alpha latent variables (firm value, profitability and capital structure) are more than 0.6, according to the criteria of reliability validity. Based on the results of processing validity reliability in Table 5, it can be concluded that the indicator is reliable/consistent measuring the latent variables.

Tabel 5: Reability Validiy

Composite Reliability

Cronbachs Alpha

Firm Value

0,834

0,631

Profitability

0,891

0,804

Capital Structure

0,957

0,917

Sumber: Data dioleh dengan Smart-PLS 2.0

Tabel 6: Inner Model

Relationship of

Latent Variables

Path Coeficient

T Statistics

Descrption

Profitability -> Firm Value

0,35

4,80

Signifikan

Profitability -> Capital Structure

0,24

2,38

Signifikan

Capital Structure -> Firm Value

0,36

1,97

Signifikan

Sumber. Data Diolah dengan Smart-PLS 2.0

Tables 1-5 inform that all indicators are valid and reliable for their latent variables, which means that PBV and PER are able to measure the value of a company's property and real estate well. ROA and NPM are able to measure the profitability of property and real estate companies. DER and DAR are able to measure properly the capital structure of property and real estate companies. After each indicator is able to properly measure its latent variables, an inner model analysis is performed to see the significance of the relationship between the latent variables and to test the hypothesis that has been made.

Inner Model

The inner model in this study is used to see the significance of the path/relationship between latent variables and to test the hypothesis that has been made. A path is said to be significant if the Tstatistic value>1.96. The results of processing using the Smart-PLS 2.0 software are presented in Table 6 as follows:

Table 6 informs that all Tstatistic values are more than 1.96, this shows that all paths are significant. Based on Table 6 it can be concluded that Hypothesis 1 is accepted, which means that profitability affects the value of the company. Hypothesis 2 is accepted which means that profitability affects the capital structure. Hypothesis 3 is accepted, which means that capital structure influences firm value. To see whether hypothesis 4 is accepted or not, one of the mediation test methods must be used. Mediation test in research uses the Variance Accounted For (VAF) test).

Variance Accounted For (VAF)

A variable as a mediating variable if the VAF value is more than 20%. Based on Table 6 and Figure 2 we can calculate VAF values as follows:

The direct effect of profitability on firm value = 0,347

The indirect effect of profitability on firm value through capital structure = 0,237 * 0,364 = 0,087

The effect of total profitability, capital structure on the value of the company = 0,087 + 0,347 = 0,434

Based on direct and indirect effects on numbers 1 to 3, the VAF values can be written as follows:

Based on the VAF value above, VAF value> 20%, this shows that the capital structure as a partial mediating variable in the relationship of profitability to firm value, it can be concluded that hypothesis 4 is accepted which means the capital structure mediates the relationship of profitability to firm value.

DISCUSSION

The Effect of Profitability on Firm Value

The path coefficient in this study shows the profitability value of the Firm Value is 0.35 while the t-statistic value is 4.79763>1.96. These results indicate that profitability has a significant positive effect on Firm Value, so the first hypothesis can be accepted. The higher the value of the company's profitability, the greater the impact on the firm value. This is because if a company's profit has a relatively large value, it can provide a positive signal for investors to invest their funds in the company. This investor interest can have an impact on increasing the company's stock price. The increase in the company's stock price will have an impact on increasing the Firm Value. These results are in accordance with the signaling theory.

The results of this study were supported by Lumoly et al. [32]. The higher the growth of a company's profitability, it reflects good prospects in the future. If a company is able to increase company profits, it will have an impact on increasing the company's share price, so that it can increase Firm Value. This is because the prospect of the company in the eyes of investors is getting better [33]. Yanti and Darmayanti [34] said that if Firm Value increases, it can have an impact on the high rate of return obtained by investors. The high and low rate of return on investment results can be influenced by the size of the profit generated. Zuhroh [21] states that the high profit earned by the company shows good prospects, especially in the morning for potential investors to invest their funds, because the size of the profit will have an impact on the investment returns obtained and also have an impact on increasing Firm Value.

The Effect of Profitability on Capital Structure

The path coefficient in this study shows the profitability value of the capital structure of 0.468 while the t-statistic value is 2.565>1.96. This shows that the capital structure has a significant positive effect on profitability, so that the second hypothesis can be accepted. The greater the profitability of a company, the greater the capital structure. These results indicate that if the company earns a large profit and is used to develop its business, it is still lacking, the company can finance through debt to fund the company's operational activities, especially if the company is engaged in the Real Estate and Property sector. This is often done through credit sales. If a company can maximize the funds obtained from debt optimally, it can later generate operating profits.

The results of this study are supported by Niresh and Velnampy [34] and Purwohandoko [7]. These results indicate that the greater the profitability can increase the size of the capital structure. The capital structure is long-term funding in the form of own capital and long-term debt, the capital can be allocated as a source of funding to finance investment activities that will be carried out by the company. If a company utilizes retained earnings to finance investment activities, the alternative can be through debt [35].

The Effect of Capital Structure on Firm Value

The path coefficient in this study shows the value of the capital structure to the firm value of 0.326 while the t-statistic value is 2.098>1.96. These results indicate that the capital structure has a significant positive effect on Firm Value, so that the third hypothesis is accepted. The larger the company's capital structure, the greater the Firm Value. This is because if a company finances its business through debt and the debt used by the company is still at an optimal point, the funding if managed effectively and efficiently will be able to generate operating profit. An increase in a company's operating profit indicates a positive signal for investors to invest in the company, so the increase in investors who will invest will have an impact on increasing the company's stock price and will have an impact on Firm Value. Companies that use debt can also minimize the imposition of taxes, so that the tax burden that will be charged by the company tends to decrease. It is possible that the decrease in costs can increase profits and have an impact on increasing Firm Value. These results are in accordance with the Trade Off theory, which states that the use of high debt will be able to reduce the taxation of Brigham et al. [36].

The results of this study are supported by Masulis Research [37], Chowdhury [38], Antwi et al. [28] and Fernandes Moniaga [39] show that capital structure has a significant positive effect on firm value. High capital structure can affect the high firm value. Companies in making funding decisions through the capital structure must be optimal. The capital structure can be said to be optimal if it can minimize the cost of capital and maximize the value of the company. According to MM theory, it states that the increased use of debt in financing the company's operational activities will be able to increase firm value, if it reaches the optimal point, this is reinforced by the trade-off theory which states that the use of debt can reduce tax costs and company agency costs [12].

Capital Structure mediates the effect of Profitability on Firm Value

The results of this study in determining mediation using the VAF value. VAF value>20%, it can be concluded that capital structure as a mediating variable can partially mediate the relationship between profitability and Firm Value, so hypothesis four can be accepted. Profitability can directly affect Firm Value. In addition, indirectly, the capital structure also has a great influence on profitability and firm value. In companies that have high profitability, investors also continue to consider increasing the Firm Value of the company that is the object of investment. The results of this study are supported by research conducted by Hermuningsih [9].

CONCLUSION

The results showed that NPM and ROA were able to measure profitability. DAR and DER are able to measure capital structure. PBV and PER are able to measure the value of the company. The results showed that all hypotheses were accepted which meant that profitability affected the capital structure, capital structure influenced the value of the company, capital structure affected the value of the company. Mediation test shows that capital structure is a mediating variable between profitability and firm value. The company must be able to increase profitability so that it can increase capital structure which will have an impact on increasing firm value. Future studies can explore and expand research on the effect of capital structure on firm value with a variety of different indicators such as dividend yield, dividend payout ratio and other indicators for corporate financial performance variables and extend the research period to obtain more representative results.

REFERENCES

Andini, N.W.L. and N.G.P. Wirawati. "The effect of cash flow on financial performance and its implications on the value of manufacturing companies." Udayana University Accounting E-Journal, vol. 7, no. 1, 2014.

Noerirawan, R. et al. "The influence of the company's internal and external factors on company value." Journal of Accounting, vol. 1, no. 2, 2012.

Soliha, Euis and Taswan. "Influence of debt policy on value the company and some of the factors that influence it." Business Journal and Economics, vol. 9, no. 2, 2002.

Mahendra, Alfredo. "The influence of financial performance on firm value (dividend policy as moderating variable) in manufacturing companies on the IDX." Udayana University, 2011.

Riyanto, Bambang. Fundamentals of corporate spending. 4th ed., BPFE Yogyakarta, 2010.

Suffah and Ridwan. "The effect of leverage, profitability, dividend yield and firm size on firm value." Journal of Accounting Science and Research, vol. 5, no. 2, 2016.

Purwohandoko. "The influence of firm’s size, growth and profitability on firm value with capital structure as the mediator: A study on the agricultural firms listed in the Indonesian Stock Exchange." International Journal of Economics and Finance, vol. 9, no. 8, 2017, p. 103, doi:10.5539/ijef.v9n8p103.

Sucuahi, W. and J.M. Cambarihan. "Influence of profitability to the firm value of diversified companies in the Philippines." Accounting and Finance Research, vol. 5, no. 2, 2016, p. 149, DOI:10.5430/afr.v5n2p149.

Hermuningsih. "The effect of profitability, size, on firm value with capital structure as an intervening variable." Journal of Business Strategy, ISSN 0853-7666, 2012.

Thaib and A. Dewantoro, I. "The effect of liquidity and profitability on firm value with capital structure as intervening variable." Journal of Management Banking and Accounting, vol. 1, no. 1, 2017.

Sudana, I.M. Corporate financial management theory & practice. Erlangga, 2011.

Brigham, E.F. and J.F. Houston. Fundamentals of financial management. 10th ed., translation, Salemba Empat, 2006.

Hanafi, Mamduh M. Financial management. 2nd ed., 3rd printing, BPFE Yogyakarta, 2018.

Martono and Agus Harjito. Financial management. 5th ed., Econisia, 2005.

Sartono, Agus. Financial management theory and application. BPFE Yogyakarta, 2005.

Besley, Scott and Eugene F. Brigham. Principles of finance. The Dryden Press, Harcourt Brace Colleges Publishers, 2001.

Toto, Prihadi. Quick detection of financial conditions: 7 financial ratio analysis. Printing 1, PPM, 2008.

Saidi. "Factors affecting capital structure in manufacturing companies go public on the JSE 1997–2002." Journal of Business and Economics, vol. 11, no. 1, 2004, pp. 44–58.

Sari, Devi Verena and A. Mulyo Haryanto. "Effect of profitability, asset growth, company size, asset structure and liquidity on capital structure in manufacturing companies on the Indonesia Stock Exchange in 2008–2010." Diponegoro Journal of Management, vol. 2, no. 3, 2013, pp. 1.

Fahmi, Irham. Analysis of financial statements. Alphabeta, 2015.

Zuhroh, I. "The effects of liquidity, firm size and profitability on the firm value with mediating leverage." KnE Social Sciences, 2019, doi:10.18502/kss.v3i13.4206.

Myers, S.C. "Determinants of corporate borrowing." Journal of Financial Economics, vol. 9, no. 3, 1997, pp. 237–264.

Weston, J.F. and Thomas E.C. Financial management. Vol. 1, translated by Jaka Wasana and Kibrandoko, Binarupa Aksara, 1997.

Van Horne, James C. and John M. Wachowicz. Principles financial management. 13th Ed., Salemba Empat, 2012.

Tandelilin, Eduardus. Investment analysis and portfolio management. 1st ed., BPFE, Yogyakarta, 2001.

Yanti, I.G.A.D.N. and N.P.A. Darmayanti. "The effect of profitability, firm size, structure capital and liquidity to the value of food and beverage companies." Management E-Journal Udayana University, 2019, DOI:10.24843/ejmunud.2019.v08.i04.p15

Modigliani, F. and M.H. Miller. "The cost of capital, corporation finance and the theory of investment." American Economics Review, vol. 13, no. 3, 1963, pp. 261–297.

Antwi, Samuel, et al. "Capital structure and firm value: Empirical evidence from Ghana." International Journal of Business and Social Science, 2012.

Adelegan and Radzewicz-Beeck. "What determines bond market development in sub-Saharan Africa?" International Monetary Funds Working Paper, 2009.

Mardalis. Research strategy: A proposal approach. Earth Literacy, Jakarta, 2007.

Chin, W.W. "The partial least squares approach for structural equation modeling." In G. A. Marcoulides (Ed.), Modern methods for business research, Lawrence Erlbaum Associates, 1998, pp. 295–236.

Lumoly, Selin, Sri Murni and Victoria N. Untu. "Effect of liquidity, company size and profitability to firm value." Journal Research in Economics, Management, Business and Accounting, vol. 6, no. 3, 2018, pp. 1108–1117.

Husnan, Suad. Portfolio theory and securities analysis. UPP AMP YKPN, Yogyakarta, 2009.

Niresh, J. Aloy and T. Velnampy. "Firm size and profitability: A study of listed manufacturing firms in Sri Lanka." International Journal of Business and Management, vol. 9, no. 4, 2014, pp. 57–64.

Harahap, S.S. Analysis of financial statements. Kris, Raja Grafindo Persada, Jakarta, 2008.

Brigham, Eugene F. and Joel F. Houston. Fundamentals of financial management. 11th ed., Erlangga, Jakarta, 2011.

Masulis, R.W. "The effect of capital structure change on security prices: A study of exchange offers." Journal of Financial Economics, vol. 8, no. 2, 1983, pp. 139–178.

Chowdhury, Anup and Suman Paul Chowdhury. "Impact of capital structure on firm's value: Evidence from Bangladesh." Business and Economic Horizons, vol. 3, 2010.

Fernandes, Moniaga. "Capital structure, profitability and cost structure on the value of ceramic, porcelain and K industrial companies." 2013.

Advertisement

Recommended Articles

Research Article

Modelling Structure Job Quality, Job Design and Job Satisfaction

Moch Nurhadi,

...

Avi Sunani

Published: 30/08/2022

Download PDF

Cite

x

APA

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. & Sunani, A. (2022). Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management, 3(2), 1-4.

MLA

Nurhadi, Moch, et al. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3.2 (2022): 1-4.

Chicago

Nurhadi, Moch, Moch Bisyri Effendi, Achmad Saiful Ulum and Avi Sunani. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3, no. 2 (2022): 1-4.

Harvard

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. and Sunani, A. (2022) 'Modelling Structure Job Quality, Job Design and Job Satisfaction' Himalayan Journal of Economics and Business Management 3(2), pp. 1-4.

Vancouver

Nurhadi M, Bisyri Effendi M, Saiful Ulum A, Sunani A. Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management. 2022 Jul;3(2):1-4.

Download PDF

Research Article

Accountability and Transparency of Village Fund Management in Lumajang District

Nurina Ayuningtiyas,

...

Muhammad Miqdad

Published: 28/12/2023

Download PDF

Cite

x

APA

Ayuningtiyas, N., Santosa Putra, H. & Miqdad, M. (2023). Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management, 4(2), 1-4.

MLA

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4.2 (2023): 1-4.

Chicago

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4, no. 2 (2023): 1-4.

Harvard

Ayuningtiyas, N., Santosa Putra, H. and Miqdad, M. (2023) 'Accountability and Transparency of Village Fund Management in Lumajang District' Himalayan Journal of Economics and Business Management 4(2), pp. 1-4.

Vancouver

Ayuningtiyas N, Santosa Putra H, Miqdad M. Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management. 2023 Jul;4(2):1-4.

Download PDF

Research Article

Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya

Kinisu Sifuna,

...

Peter Simotwo

Published: 30/06/2021

Download PDF

Cite

x

APA

Sifuna, K., Lwangale, D. W., Simotwo, P., Sifuna, K., Lwangale, D. W. & Simotwo, P. (2021). Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya. Himalayan Journal of Economics and Business Management, 2(1), None-None.

MLA

Sifuna, Kinisu, et al. "Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya." Himalayan Journal of Economics and Business Management 2.1 (2021): None-None.

Chicago

Sifuna, Kinisu, David W. Lwangale, Peter Simotwo, Kinisu Sifuna, David W. Lwangale and Peter Simotwo. "Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya." Himalayan Journal of Economics and Business Management 2, no. 1 (2021): None-None.

Harvard

Sifuna, K., Lwangale, D. W., Simotwo, P., Sifuna, K., Lwangale, D. W. and Simotwo, P. (2021) 'Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya' Himalayan Journal of Economics and Business Management 2(1), pp. None-None.

Vancouver

Sifuna K, Lwangale DW, Simotwo P, Sifuna K, Lwangale DW, Simotwo P. Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya. Himalayan Journal of Economics and Business Management. 2021 Jan;2(1):None-None.

Download PDF

Research Article

The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022

Fathurrozi Azhar Edyansyah,

...

Agung Budi Sulistiyo

Published: 05/07/2025

Download PDF

Cite

x

APA

Azhar Edyansyah, F., Prasetyo, W. & Budi Sulistiyo, A. (2025). The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022. Himalayan Journal of Economics and Business Management, 6(2), 1-4.

MLA

Azhar Edyansyah, Fathurrozi, Whedy Prasetyo and Agung Budi Sulistiyo. "The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022." Himalayan Journal of Economics and Business Management 6.2 (2025): 1-4.

Chicago

Azhar Edyansyah, Fathurrozi, Whedy Prasetyo and Agung Budi Sulistiyo. "The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022." Himalayan Journal of Economics and Business Management 6, no. 2 (2025): 1-4.

Harvard

Azhar Edyansyah, F., Prasetyo, W. and Budi Sulistiyo, A. (2025) 'The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022' Himalayan Journal of Economics and Business Management 6(2), pp. 1-4.

Vancouver

Azhar Edyansyah F, Prasetyo W, Budi Sulistiyo A. The Effect of Return on Investment (Roi) as a Decision-Making Instrument on The Share Value of Food and Beverage Companies Listed on The Bei for the Period 2021-2022. Himalayan Journal of Economics and Business Management. 2025 Jul;6(2):1-4.

Saiful Ulum, A. (2022). Determinants of Firm Value on Real Estate and Property Sector. Himalayan Journal of Economics and Business Management, 3(1), 1-8.

MLA

Saiful Ulum, Achmad. "Determinants of Firm Value on Real Estate and Property Sector." Himalayan Journal of Economics and Business Management 3.1 (2022): 1-8.

Chicago

Saiful Ulum, Achmad. "Determinants of Firm Value on Real Estate and Property Sector." Himalayan Journal of Economics and Business Management 3, no. 1 (2022): 1-8.

Harvard

Saiful Ulum, A. (2022) 'Determinants of Firm Value on Real Estate and Property Sector' Himalayan Journal of Economics and Business Management 3(1), pp. 1-8.

Vancouver

Saiful Ulum A. Determinants of Firm Value on Real Estate and Property Sector. Himalayan Journal of Economics and Business Management. 2022 Jan;3(1):1-8.