This study aimed to investigate the effects of unemployment and inflation on economic growth in Sri Lanka for the period of 1990 - 2016. Annual time series data, sourced from the World Bank Development Indicators, were employed for the empirical analysis. This study used Augmented Dickey Fuller Test to test the stationary properties of the timeseries variables while Long-run and short-run elasticities of the variables were examined using the Autoregressive Distributed Lag (ARDL) Bounds test co-integration method. The unit root test results indicate that economic growth and inflation are stationery on level but unemployment is stationery after being differenced one. The ARDL bounds test results confirm that a long-run co-integrating relationship exists among inflation, unemployment and GDP growth rate. The estimated empirical results showed that Unemployment and GDP growth rate have a strong negative significant relationship whereas Inflation and GDP growth rate have a positive significant relationship in the long-run.

Keywords

Inflation

Unemployment

Economic Growth

ARDL

Bounds testing

Sri Lanka.

INTRODUCTION

The relationship between inflation, unemployment and economic growth has long been a fundamental question in economics. Many countries in the world find it difficult to manage higher rates of Unemployment and inflation which have been an issue of concern, most especially in developing countries like Sri Lanka, to policymakers and researchers. This is because unemployment and inflation are widely used as important macroeconomics indicators and determinants of economic growth and development. Economic growth can be defined as the increase in the inflation- adjusted market value of the goods and services produced by an economy over time. It is conventionally measured as the percentage of increase in real gross domestic product. Unemployment means unable to get a job even for those who are willing and able to work at the prevailing wage and working conditions. According to the International Labor Organization (ILO), unemployment is a situation in which people are actively seeking work for the past four weeks but they are unable to find work. A persistent increase in the general price level of goods and services in a country or the continuous decline in the purchasing value of money over a specific time period is defined as inflation.

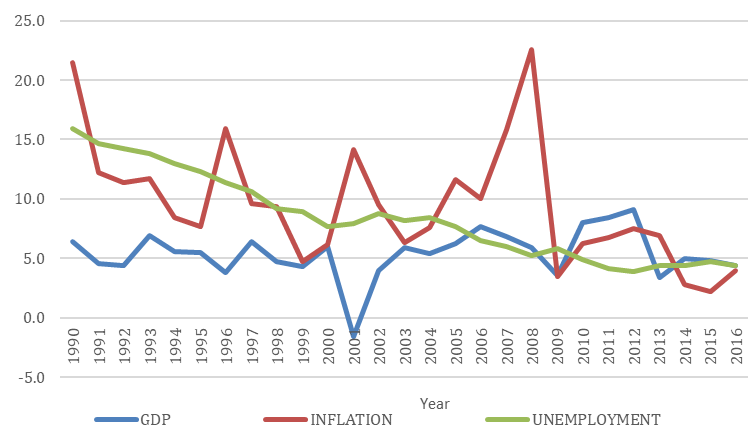

After Sri Lanka’s economy turned into an open economy in 1977, unemployment and inflation started to increase in two digits. As a result, the Sri Lankan economy faces many structural changes in various aspects. The unemployment rate which recorded the highest rate of 15.9 percent in 1990, declined gradually until 2000 and reached 7.7 percent in that same year. After that, it increased further and recorded an 8.8 percent rate of unemployment in 2002. Again from 2003, it started to decline and recorded 5.2 percent in 2012. However, it increased a little in 2009 as 5.8 percent during the end of the civil war. Then it started to decline continuously until 2012 and reached the lowest rate of 3.9 percent in that year. However, it increased further from 2013 with a rate of 4.4 percent and recorded 4.7 percent in 2015. After that it declined a little and recorded 4.4 percent in 2016.

Beside unemployment, inflation which was measured by consumer prices index (CPI) is another important macroeconomic problem which affects both economic and social indicators in the country. Sri Lankan economy has also come across with this macroeconomic issue and the inflation rate was recorded 21.5 percent in 1990 and here after it was reported the highest rate of 22.6 in 2008. Then it declined rapidly in 2009, during the end of the civil war and it was controlled in one digit. Then, it increased again and reported 7.5 percent in 2012. Aftermath, it started to decrease further until 2015 and recorded the lowest rate of 2.2 percent in 2015. Then, it began to increase sharply and recorded 4 percent in 2016. GDP growth rate is used as a proxy for economic growth in this study and it is generally perceived that when economic growth takes place in the country, it increases the pace of Beside unemployment, inflation which was measured by consumer prices index (CPI) is another important macroeconomic problem which affects both economic and social indicators in the country. Sri Lankan economy has also come across with this macroeconomic issue and the inflation rate was recorded 21.5 percent in 1990 and here after it was reported the highest rate of 22.6 in 2008. Then it declined rapidly in 2009, during the end of the civil war and it was controlled in one digit. Then, it increased again and reported 7.5 percent in 2012. Aftermath, it started to decrease further until 2015 and recorded the lowest rate of 2.2 percent in 2015. Then, it began to increase sharply and recorded 4 percent in 2016. GDP growth rate is used as a proxy for economic growth in this study and it is generally perceived that when economic growth takes place in the country, it increases the pace of economic activity in the country, due to the employment increases. The increase in employment opportunities will enhance the purchasing power of the people in the country and as a result, consumption increases which leads to raise aggregate demand and hence inflation in the country.

Figure 1: Trend of unemployment, inflation and Economic growth rate, 1990-2016

Source: World Bank database, World Development Indicators, 1990- 20161

In Sri Lankan context, GDP growth rate was reported 6.4 percent in 1990 and it showed a negative growth rate at 1.5 percent in 2001. It reached a growth rate of 3.5 percent in 2009 during the end of the civil war. After that, it started to increase until 2012 and recorded the peak of 9.1 percent in 2012. Then, it started to decline again in 2013 and recorded 3.4 percent in 2013. Aftermath, it increased again from 2014 and recorded 4.4 percent economic growth in 2016. Likewise, the rate of unemployment and inflation fluctuates time to time. As a result of this it affects the economic growth and development of our country. The various macroeconomic policies, implemented by the Sri Lankan government have been unable to achieve desired goals of price stability, reduction in unemployment and sustained economic growth. The fluctuations in the economy have confirmed the need to manage the economy effectively and steadily.

The objective of this study is to investigate and determine the effects of unemployment and inflation on economic growth in Sri Lanka between the period of 1990-2016 and the existence of a long- run relationship between unemployment and inflation with GDP growth rate in Sri Lanka.

Literature review

There is a large number of empirical studies trying to identify the controversial relationship between economic growth, unemployment and inflation in different economies of the world.

Jaradat [2] examined the effect of inflation and unemployment on Jordanian GDP during the period of 2000 to 2010. The results of the Linear Regression Method carried-out in this study revealed a negative relationship between unemployment and GDP, and a positive relationship between Inflation and GDP in Jordan. Similarly, Li and Liu [3] used annual time series data from 1978 to 2010 to investigate the controversial relationship among unemployment rate, inflation rate and economic growth rate of China. The study employed Granger causality test to detect the casual relationship, unit root test for testing the stationary of the series, co-integration test, Vector Auto Regressive (VAR) and Vector Error Correction (VEC) models. The empirical results confirmed that there is a long-term stable equilibrium relationship among the variables. The findings of this study also revealed that unemployment impacted negatively on economic growth while inflation impacted positively on economic growth in China.

Umar and Zubairu [4] conducted research to find out the controversial relationship between inflation and the economic growth of the Nigerian economy for the period of 1970 to 2010. This study employed Augmented Dickey-Fuller (ADF) unit root test to check for the stationarity properties of the variables in this study. The empirical results revealed that inflation had a negative impact on economic growth in Nigerian economy. Similarly, Ayyoub [5] conducted a study to analyze the impact of inflation on economic growth in the economy of Pakistan, using annual time-series data from 1972 to 2010. The study employed the Ordinary Least Squares (OLS) method for the empirical analysis and it was found that there was a negative and significant relationship between inflation and economic growth in the economy of Pakistan.

Abdul-Khaliq et al. [6] empirically examined the relationship between unemployment and GDP growth in nine Arab Countries for the period of 1994 and 2010. This study used the pooled panel unit root tests in testing the stationery of the variables and the Pooled EGLS (Cross-section SUR) estimation methods to test the relationship between the variables. The study concluded that economic growth has a significant negative effect on the unemployment rate.

Gandelman & Murillo [7] investigated the impact of inflation and unemployment on subjective personal and country evaluations. Gallup world poll data is used in this study and the data consists of citizens in a number of countries in the world. In this study, the data set of Gallup World poll data contain responses from about 70,000 individuations in 75 countries for the year 2006. The study employed Ordinary Least Square method on country level and it was found that impact on well-being from a 1%-point change in either inflation or unemployment. The overall findings of this study revealed that inflation and unemployment have a negative impact on the personal individual assessments of past and present well-being for themselves and their country.

Alias et al. [8] used data spanning the period between 1982 and 2008 to examine the correlation between Inflation Rate and Employment Rate with Gross Domestic product in Malaysia. This study applied the unit root test for stationary, Johansen Cointegration test and Granger Causality test. The unit root test reveals that all variables have become stationary after being differenced one. The Johansen Cointegration test results confirm the long-run cointegrating relationship and it also shows that GDP and the explanatory variables moves closely to achieve the long run equilibrium.

Shahid [9] analyzed the impact of inflation and unemployment on economic growth in Pakistan, using the time series data between the period of 1980 to 2010. This study employed the Autoregressive-Distributed Lag (ARDL) model to find out the long-run cointegrating relationship between the variables. This study also used both the ADF and Phillips-Perron (P-P) unit root techniques. The unit root test results indicate that only GDP growth rate is stationary at level while unemployment and inflation are stationary became stationary at their first difference. The result of the ARDL model carried out in the study revealed that long run cointegrating relationships exist between unemployment, inflation and economic growth. The ARDL long-run estimation results concluded that Unemployment has significant negative impact on GDP while inflation has negative but insignificant impact on GDP in the long-run in the economy of Pakistan.

Khan et al. [10] examined the inter-relationship between Gross Domestic Product (GDP) Growth and Unemployment in the country of Pakistan. The empirical study used the annual time series data during the period of 1960 to 2005. The study initially used the Augmented Dickey-Fuller (ADF) unit root test to examine the stationary of the time series variables. All the variables which were non- stationary at level made stationary after taking the first difference. Johansen Cointegration test was also used to ascertain the co-integration in the regression. The findings of this study revealed that GDP growth rate has a significant negative relationship with Unemployment in the long-run.

Thayaparan [11] examined the effect of inflation and economic growth on unemployment in Sri Lanka. The study used the annual time series data sourced from the annual reports of the Central Bank of Sri Lanka (CBSL) for the period of 1990- 2012. This study employed the Augmented Dickey Fuller (ADF) Test to test stationary of the series and Granger Causality test to detect the causal relationship between the variables. Results of the unit root test indicate that only Gross Domestic Product (GDP) is stationary on level while unemployment and inflation are stationary at their first difference. The overall results of this study concluded that inflation has a significant negative impact on unemployment whereas gross domestic product positively but insignificantly affects the unemployment in Sri Lanka.

Ademola & Badiru [12] empirically investigated and determined the controversial relationship between unemployment, inflation and economic growth within the Nigerian context using annual time series data from 1981 to 2014. This study carried out both Augmented Dickey-Fuller (ADF) and Phillips-Perron (P-P) unit root tests to check the stationary properties of the time series variables. The unit test results confirmed that all the variables are stationary at first difference. The Johansen cointegration test was also used in this study to test the long-run relationship between the variables and the results revealed that there is a long-run relationship among the variables in the model. The empirical results concluded that both unemployment and inflation have a positive impact on economic growth in Nigeria.

Empirical analysis

Data and Selection of Variables: This study assessed the impact of unemployment and inflation on economic growth in Sri Lanka using the annual time series data for the period between 1990 and 2016. The data which were employed in this study sourced from the World Bank Development Indicators (2017) for the above research period. The annual data of GDP Growth rate was used as target Variable while Inflation rate and Unemployment rate were used as explanatory variables. In this study, the data of economic growth is obtained as the rate of change in real Gross Domestic Product (GDP). Unemployment rate is obtained as the rate of unemployed people is divided by the total number of people in the labour force in Sri Lanka, while inflation rate is measured by Colombo Consumer Price Index (CCPI) of Sri Lanka.

Empirical Model: This study adopted the Okun’s [13] type model which was proposed by Okun in 1962 in his working paper. In our study, this model is modified in order to include unemployment and inflation as the independent variables while economic growth as the dependent variable and it is proxied by the real GDP growth rate. The Okun’s law is the reduced form of the Phillips postulate and assumes a linear relationship between the GDP growth rate, the rate of unemployment and inflation rate and it is presented as follows,

RGDP = f (INFLA, UNEMP)

(1)

Thus, the econometric model can be specified as follows:

where RGDP represents the real GDP growth rate of Sri Lanka. INFLA indicates the rate of inflation and UNEMP represents the rate of unemployment of Sri Lanka. β0 is intercept. β1 and β2 are slope coefficients. εt is white noise error term and t represents the time period (t =1, 2, .,T). All the variables are converted into natural logarithm which is denoted by ln in the above function.

Unit Root Analysis

The initial step in time series modeling is to identify the degree of integration of the variables in interest. Most of the macroeconomic series are found to have unit roots as they are not stationary or their variances increase with time. Thus, the unit root test is the formal method to test the stationary of a time series data. If a variable is non-stationary, it has a unit root meaning there is a problem of spuriousness if the regression is to be estimated using the ordinary least squares (OLS). Therefore, it is necessary to check the stationary properties of the time series variables before estimating the ARDL model.

Moreover, stationary test is required in this study to confirm that none of the variables follow I (2) of integration because cointegration relationship can be performed using ARDL Bounds test method when the variables have integrated order of I (0), I (1) or combination of both. In this study, the unit root test is performed by using the Augmented Dickey Fuller 14 (ADF) test.

The unit root test results which are shown in Table 2 confirms that none of the variables follow I (2) order of integration and the selected variables are integrated into orders either I (1) or I (0). The results further revealed that both real GDP growth rate and inflation rate are stationary at level (I (0)) while unemployment rate is non-stationary at level made stationary after taking the first difference, indicating I (1) order of integration.

ARDL Bounds Test Approach

The Autoregressive Distributed Lag (ARDL) Bounds testing approach is carried out in this study to test the existence of a long-run cointegrating relationship among the variables. The ARDL which was suggested by Pesaran and Shin15 and extended by Pesaran et al. [16], helps to find-out the long-run equilibrium and the long-run and short-run dynamic relationship between the nonstationary time series variables [17]. ARDL approach is employed because this method has some advantages and flexibilities when it is compared to other alternatives methods such as Engle and Granger18, Johansen19, and Johansen and Juselius20 procedures. First, it has more power and it is recommended to apply to a small sample size study (Pesaran et al.16; Ghatak & Siddiki21; Acaravci & Ozturk22) and therefore conducting bounds testing will be appropriate for the present study.

One of the important flexibilities of the ARDL bounds test approach is its usability when not all variables have the same order of integration. According to this method, the existence of a co-integration relationship can be investigated between the time-series regardless of whether the underlying variables are I (0), I (1) or mutually integrated and this point is the greatest merit of the bounds test than other conventional co-integration testing.

After reviewing the above advantages, the equation (2) is formulated as below to identify the existence of long-run relationship among the variables:

Where α0 is constant, α1, α2 and α3 are the short-run dynamic coefficients, whereas δ1, δ2 and δ3 are the long-run coefficients, Δ denotes first difference and εt1 is white noise error term.

The first step in the ARDL bounds testing approach is to estimate Equation (3) by ordinary least squares in order to test for existence of a long-run relationship among the variables by conducting an F-test for the joint significance of the coefficients of the lagged level variables. The existence of the long-run relationship between the variables is confirmed by the bound F- statistic.

Table 1. Unit root test results

Variable

Test Statistic at level

Test Statistic at first difference

Lag

Critical value

Order of integration

P - Value

1%

5%

10%

RGDP

-4.279

-

0

-3.743

-2.997

-2.629

1(0)***

0.0005

INFLA

-4.053

-

0

-3.743

-2.997

-2.629

1(0)***

0.0012

UNEMP

-2.530

-4.458

0

-3.743

-2.997

-2.629

1(1)***

0.0002

*, **, *** represent 10%, 5% and 1% levels of significant respectively

A bounds F- test is actually a test of the hypothesis of no cointegration among the variables (H0: δ1= 0, δ2=0, δ3 = 0) against the existence of cointegration among the variables (H1: δ1≠ 0 or δ2≠ 0 or δ3 ≠ 0). Two sets of critical value bounds for the F- statistic are generated by Pesaran et al16 for the different model specification: the upper bound applies when all variables are integrated of order one, I (1) and the lower bound applies when all the variables are stationary, I (0).

If the computed F-statistic falls below the lower bound critical value, the null hypothesis of no-cointegration cannot be rejected, indicating there is no long-run relationship existing among the variables. Contrary, if the computed F-statistic lies above the upper bound critical value; the null hypothesis is rejected, implying that there is a long-run cointegration relationship among the variables in the model. Nevertheless, if the calculated F-statistic lies between the lower and the upper bounds, conclusive inference may not be made.

After detecting the existence of cointegrating relationship by using bounds F statistic in the above model, the long run coefficients of the ARDL model for can be estimated. As a final step, we obtain the short-run dynamic parameters by estimating an Error Correction Model (ECM). The ECM gives the results of a short-run dynamic relationship between the variables (Emika and Aham23). Thus, equation (3) can be further transformed as in equation (4) to accommodate the error correction term with one period lagged:

Where, ∅ is the speed of adjustment parameter which should have statistically significant and negative sign to support the co-integration between the variables and μ_t is the pure random error term.

RESULTS

Empirical Results and Discussion

ARDL Bounds Test Cointegration Results: Once we determine the order of integration of the macro-economic variables employed in this study, it is important to determine the existence of a long-run relationship among the variables. Since, the unit root analysis clearly shows that the variables are integrated order at I(1) and I(0) or mix order, it is appropriate to employ the ARDL Bounds test approach in order to determine the long-run cointegrating relationship among the variables. Table 2 clearly represents the results of the ARDL Bounds F-test to identify the cointegrating relationship among the variables. The results of the Bounds test approach confirm the existence of a long-run relationship among the variables unemployment rate, inflation rate and GDP growth rate. The results reveal that the computed F-statistics of 6.287 is obviously higher than the upper bound critical value at the 5% significant level. Thus, the null hypothesis of no cointegration is rejected, indicating there is a stable long-run cointegrating relationship between the variables unemployment, inflation and economic growth rate.

Results of Short-run and Long-run ARDL Estimated Model

After determining the cointegration status of the specified model, it is important to proceed the estimation of the short-run and long-run ARDL model. The long-run estimated coefficients of the ARDL model is displayed in table 3. According to the results of ARDL in the long-run, Unemployment (UNEMP) has a negative significant impact on GDP whereas inflation (INFLA) has a positive significant impact on GDP. The estimated long-run coefficient of unemployment rate is -0.233, indicating a percent increase in unemployment decreases the Growth rate by 0.23%. Thus, the higher unemployment rate tends to reduce Sri Lanka’s real economic growth rate in the long-run, as expected. The long-run coefficient of unemployment is statistically significant at 1% level of significance as indicated by their P-values (0.001). On the other hand, the estimated long-run coefficient of inflation is 0.211. It means that a 1% increase in inflation accelerates the Growth rate by 0.21%. The coefficient of inflation is also statistically significant at 1% level of significance as indicated by their P-values (0.008). The findings of this study are consistent with the findings of Jaradat, Li and Liu, Umar and Zubairu and Abdul-Khaliq et al. [2,3,4,6].

Table 2: Ardl bounds test for the existence of cointegration (unrestricted intercept & no trend)

Test Statistics

Test values

10% critical value

5 % critical value

1% critical value

I(0)

I(1)

I(0)

I(1)

I(0)

I(1)

F-statistic

6.287**

3.17

4.14

3.79

4.85

5.15

6.39

T- statistic

-4.032**

-2.57

-3.21

-2.86

-3.53

-3.43

-4.10

Note: ** indicate that the computed F statistic falls above the upper bound value at five % significant level.

Table 3: Estimated long-run coefficients based on ARDL model

Table 4: Error correction representation for the selected ARDL model

Variables

coefficient

Std. Err

t- statistic

P- value

Δ lnRGDP(-1)

2.592**

0.859

3.01

0.039

Δ lnRGDP-2)

2.243**

0.634

3.53

0.024

Δ lnINFLA

0.507

0.271

1.87

0.135

Δ lnINFLA(-1)

-0.429*

0.167

-2.56

0.063

Δ lnINFLA(-2)

0.279

0.173

1.62

0.181

Δ lnINFLA(-3)

-0.656***

0.139

-4.71

0.009

Δ lnUNEMP

4.406*

1.938

2.27

0.085

Δ lnUNEMP(-1)

-2.474**

0.831

-2.98

0.041

Δ lnUNEMP(-2)

5.067**

1.191

4.26

0.013

Δ lnUNEMP(-3)

-9.718**

2.678

-3.63

0.022

ECM (-1)

-5.348**

1.326

-4.03

0.016

R- square 0.975

Adj R- squared 0.897

*, **, *** represent 10%, 5% and 1% levels of significant respectively

Once we find out the long-run estimation results of the ARDL model, then the short-run dynamic relationship between the variables is tested by using the Error Correction Model (ECM). The results of short-run dynamics from ECM of ARDL are reported in Table 4. The short-run adjustment process is denoted by ECM (-1) coefficient in this model. The error correction coefficient -5.348 has the expected negative sign and is highly significant at 1% level, re-establish and confirming the cointegrating relationships between the variables. The estimated Error Correction term (ECM (-1)) explains how the model is adjusted towards the long-run equilibrium state after external shock. Moreover, the short-run dynamic relationships between the variables in table 4, reveal that inflation has a significant negative impact on economic growth in Sri Lanka, implying higher inflation rate tends to reduce Sri Lanka’s real economic growth rate in the short-run. The short-run dynamic coefficient of the one period and three period lagged value of inflation has the significant negative impact on real GDP growth rate at 10% and 1% level of significance respectively in the short-run. However, in the short-run, there is no clear relationship (mixed impact) between unemployment and GDP growth rate. The current and two period lagged value of unemployment exerts a significant positive relationship between unemployment and economic growth while one period and three period lagged value of unemployment shows a significant negative relationship between unemployment and the economic growth of Sri Lanka in the short-run.

CONCLUSION

This study empirically examines the effects of unemployment and inflation on economic growth in Sri Lanka for the period of 1990 – 2016. The Augmented Dickey Fuller (ADF) unit root test was conducted to test the stationary of the variables and the results reveal that the variables are integrated of orders either I(1) or I(0) (mix order of integration) and also confirms no variables follow I (2) order of integration. Thus, the ARDL bounds test approach is employed in the study to investigate the existence of a long-run relationship among the variables. The study results confirm that the long-run cointegrating relationship exists between inflation, unemployment and economic growth in Sri Lanka. The estimated empirical results indicated that Unemployment and GDP growth rate have a strong negative significant relationship whereas Inflation and GDP growth rate have a positive significant relationship in the long-run.

REFERENCE

World Bank Database. "Unemployment, percentage of total labor force (modeled ILO estimate) - Sri Lanka, inflation, consumer prices (annual percentage) - Sri Lanka, GDP growth (annual percentage) - Sri Lanka." World Bank, 2018, https://data.worldbank.org/country/sri-lanka. Accessed 18 Sept. 2019.

Jaradat, M. A. "Impact of inflation and unemployment on Jordanian GDP." Interdisciplinary Journal of Contemporary Research in Business, vol. 4, no. 10, 2013, pp. 317–334.

Li, C. S. and Z. J. Liu. "Study on the relationship among Chinese unemployment rate, economic growth, and inflation." Advance in Applied Economics and Finance, vol. 1, no. 1, 2012, pp. 1–6.

Umaru, A. and A. A. Zubairu. "Effect of inflation on the growth and development of the Nigerian economy (an empirical analysis)." International Journal of Business and Social Science, vol. 3, no. 10, 2012, pp. 183–191.

Ayyoub, M. et al. "Does inflation affect economic growth? The case of Pakistan." Pakistan Journal of Social Sciences (PJSS), vol. 31, no. 1, 2011, pp. 51–64.

Abdul-Khaliq et al. "The relationship between unemployment and economic growth rate in Arab countries." Journal of Economics and Sustainable Development, vol. 5, no. 9, 2014, pp. 56–59.

Gandelman, N. and R. Hernández-Murillo. "The impact of inflation and unemployment on subjective personal and country evaluations." Federal Reserve Bank of St. Louis Review, vol. 91, no. 3, May/June 2009, pp. 107–126.

Alias, T. S. et al. "Multivariate time series analysis on correlation between inflation rate and employment rate with gross domestic product." World Applied Sciences Journal, Special Issue on Bolstering Economic Sustainability, 2011, pp. 61–66.

Shahid, M. "Effect of inflation and unemployment on economic growth in Pakistan." Journal of Economics and Sustainable Development, vol. 5, no. 15, 2014, pp. 103–106.

Khan, A. Q. K. et al. "Inter-dependencies and causality in the macroeconomic variables: evidence from Pakistan (1960–2005)." Sarhad Journal of Agriculture (Pakistan), vol. 24, no. 1, 2008, pp. 199–205, https://mpra.ub.uni-muenchen.de/42034/.

Thayaparan, A. "Impact of inflation and economic growth on unemployment in Sri Lanka: a study of time series analysis." Global Journal of Management and Business Research, vol. 13, no. 5, 2014, pp. 45–53.

Ademola, A. and A. Badiru. "The impact of unemployment and inflation on economic growth in Nigeria (1981–2014)." International Journal of Business and Economic Sciences Applied Research, vol. 9, no. 1, 2016, pp. 47–55.

Okun, A. M. "Potential GNP: its measurement and significance." Proceedings of the Business and Economics Statistics Section of the American Statistical Association, 1962. Reprinted with slight changes in The Political Economy of Prosperity, Brookings Institution, Washington, DC.

Dickey, D. A. and W. A. Fuller. "Likelihood ratio statistics for autoregressive time series with a unit root." Econometrica: Journal of the Econometric Society, vol. 49, no. 4, 1981, pp. 1057–1072.

Pesaran, M. H. and Y. Shin. "An autoregressive distributed lag modelling approach to cointegration analysis." Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium, edited by Strom S., Cambridge University Press, 1999.

Pesaran, M. H. et al. "Bounds testing approaches to the analysis of level relationships." Journal of Applied Econometrics, vol. 16, no. 3, 2001, pp. 289–326, https://doi.org/10.1002/jae.616.

Bhavan, T. "The relationship between per capita GDP and road accidents in Sri Lanka: an ARDL bound test approach." Asian Journal of Empirical Research, vol. 8, no. 7, 2018, pp. 238–246.

Engle, R. F. and C. W. Granger. "Co-integration and error correction: representation, estimation, and testing." Econometrica: Journal of the Econometric Society, vol. 51, no. 2, 1987, pp. 251–276, https://doi.org/10.2307/1913236.

Johansen, S. "Statistical analysis of cointegration vectors." Journal of Economic Dynamics and Control, vol. 12, no. 2-3, 1988, pp. 231–254, https://doi.org/10.1016/0165-1889(88)90041-3.

Johansen, S. and K. Juselius. "Maximum likelihood estimation and inference on cointegration—with applications to the demand for money." Oxford Bulletin of Economics and Statistics, vol. 52, no. 2, 1990, pp. 169–210, https://doi.org/10.1111/j.14680084.1990.mp52002003.x.

Ghatak, S. and J. U. Siddiki. "The use of the ARDL approach in estimating virtual exchange rates in India." Journal of Applied Statistics, vol. 28, no. 5, 2001, pp. 573–583, https://doi.org/10.1080/02664760120047906.

Acaravci, A. and İ. Öztürk. "Foreign direct investment, export, and economic growth: empirical evidence from new EU countries." Romanian Journal of Economic Forecasting, vol. 2, 2012, pp. 52–67, http://www.ipe.ro/rjef/rjef2_12/rjef2_2012p52-67.pdf.

Emika, N. and K. U. Aham. "Autoregressive distributed lag (ARDL) cointegration technique: application and interpretation." Journal of Statistical and Econometric Methods, vol. 5, no. 4, 2016, pp. 63–91.

License

Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License

All papers should be submitted electronically. All submitted manuscripts must be original work that is not under submission at another journal or under consideration for publication in another form, such as a monograph or chapter of a book. Authors of submitted papers are obligated not to submit their paper for publication elsewhere until an editorial decision is rendered on their submission. Further, authors of accepted papers are prohibited from publishing the results in other publications that appear before the paper is published in the Journal unless they receive approval for doing so from the Editor-In-Chief.

Himalayan Journal of Economics and Business Management open access articles are licensed under a Creative Commons Attribution-Share A like 4.0 International License. This license lets the audience to give appropriate credit, provide a link to the license, and indicate if changes were made and if they remix, transform, or build upon the material, they must distribute contributions under the same license as the original.

Advertisement

Recommended Articles

Research Article

Modelling Structure Job Quality, Job Design and Job Satisfaction

Moch Nurhadi,

...

Avi Sunani

Published: 30/08/2022

Download PDF

Cite

x

APA

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. & Sunani, A. (2022). Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management, 3(2), 1-4.

MLA

Nurhadi, Moch, et al. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3.2 (2022): 1-4.

Chicago

Nurhadi, Moch, Moch Bisyri Effendi, Achmad Saiful Ulum and Avi Sunani. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3, no. 2 (2022): 1-4.

Harvard

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. and Sunani, A. (2022) 'Modelling Structure Job Quality, Job Design and Job Satisfaction' Himalayan Journal of Economics and Business Management 3(2), pp. 1-4.

Vancouver

Nurhadi M, Bisyri Effendi M, Saiful Ulum A, Sunani A. Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management. 2022 Jul;3(2):1-4.

Download PDF

Research Article

Accountability and Transparency of Village Fund Management in Lumajang District

Nurina Ayuningtiyas,

...

Muhammad Miqdad

Published: 28/12/2023

Download PDF

Cite

x

APA

Ayuningtiyas, N., Santosa Putra, H. & Miqdad, M. (2023). Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management, 4(2), 1-4.

MLA

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4.2 (2023): 1-4.

Chicago

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4, no. 2 (2023): 1-4.

Harvard

Ayuningtiyas, N., Santosa Putra, H. and Miqdad, M. (2023) 'Accountability and Transparency of Village Fund Management in Lumajang District' Himalayan Journal of Economics and Business Management 4(2), pp. 1-4.

Vancouver

Ayuningtiyas N, Santosa Putra H, Miqdad M. Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management. 2023 Jul;4(2):1-4.

Download PDF

Research Article

Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue

Alfarisy, K. A.,

Wandebori, H.

Published: 30/04/2024

Download PDF

Cite

x

APA

K. A., A. & H., W. (2024). Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue. Himalayan Journal of Economics and Business Management, 5(1), 1-18.

MLA

K. A., Alfarisy, and Wandebori, H.. "Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue." Himalayan Journal of Economics and Business Management 5.1 (2024): 1-18.

Chicago

K. A., Alfarisy, and Wandebori, H.. "Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue." Himalayan Journal of Economics and Business Management 5, no. 1 (2024): 1-18.

Harvard

K. A., A. and H., W. (2024) 'Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue' Himalayan Journal of Economics and Business Management 5(1), pp. 1-18.

Vancouver

K. A. A, H. W. Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue. Himalayan Journal of Economics and Business Management. 2024 Jan;5(1):1-18.

Download PDF

Research Article

The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation

Hussein Kamel Wadaa

Published: 05/05/2025

Download PDF

Cite

x

APA

Wadaa, H. K. (2025). The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation. Himalayan Journal of Economics and Business Management, 6(1), 1-10.

MLA

Wadaa, Hussein Kamel. "The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation." Himalayan Journal of Economics and Business Management 6.1 (2025): 1-10.

Chicago

Wadaa, Hussein Kamel. "The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation." Himalayan Journal of Economics and Business Management 6, no. 1 (2025): 1-10.

Harvard

Wadaa, H. K. (2025) 'The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation' Himalayan Journal of Economics and Business Management 6(1), pp. 1-10.

Vancouver

Wadaa HK. The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation. Himalayan Journal of Economics and Business Management. 2025 Jan;6(1):1-10.

Shiyalini, S. & Bhavan, T. (2021). Impact of Inflation and Unemployment on Economic Growth: The ARDL Bounds Testing Approach for Sri Lanka. Himalayan Journal of Economics and Business Management, 2(1), 1-7.

MLA

Shiyalini, S. and T. Bhavan. "Impact of Inflation and Unemployment on Economic Growth: The ARDL Bounds Testing Approach for Sri Lanka." Himalayan Journal of Economics and Business Management 2.1 (2021): 1-7.

Chicago

Shiyalini, S. and T. Bhavan. "Impact of Inflation and Unemployment on Economic Growth: The ARDL Bounds Testing Approach for Sri Lanka." Himalayan Journal of Economics and Business Management 2, no. 1 (2021): 1-7.

Harvard

Shiyalini, S. and Bhavan, T. (2021) 'Impact of Inflation and Unemployment on Economic Growth: The ARDL Bounds Testing Approach for Sri Lanka' Himalayan Journal of Economics and Business Management 2(1), pp. 1-7.

Vancouver

Shiyalini S, Bhavan T. Impact of Inflation and Unemployment on Economic Growth: The ARDL Bounds Testing Approach for Sri Lanka. Himalayan Journal of Economics and Business Management. 2021 Jan;2(1):1-7.