+91 6002993949

submission@himjournals.com

Open Access

ISSN (Print) : 2709-3549

ISSN (Online) : 2709-3557

Using a Literature Review methodology, this study focuses on identifying the methods used in the startup company valuation process and the characteristics of startup company valuation. Design/methodology/approach – Literature review based on previously conducted research studies in order to identify previously observed phenomena and cases. To gain a deeper understanding of how and which factors impact the valuation of startup companies. Findings – This study's findings consist of qualitative and quantitative valuation frameworks adapted to startups. Implications of research – It is hoped that this research can capture how startup companies are assessed and can be used as research to see how startup valuation phenomena occur. Originality/value – This paper offers new insights into the valuation of startup companies using quantitative and quantitative approaches. thereby contributing in the valuation of startup companies.

The expansion of a new company or startup is extremely rapid. Numerous businesses have developed numerous inventions and technologies that have assisted in the resolution of societal issues. The technology sector is expanding by 7%, which is twice as fast as the whole world economy [1].

As the number of companies and transactions increases, venture capital firms use a variety of approaches to value the assets of startup companies, but none of these methods are optimal for investors. Problems with the valuation of startup company assets that influence the determination of the most effective strategy.

The increase in the number of startups is followed by a rise in the number of failed or insolvent startups.Startups have the highest failure rate compared to other types of businesses. A study of 5196 Australian startup companies found that the annual failure rate was greater than 9 percent and that 64 percent of companies perished within a decade.

With a high failure rate, Investors use the valuation framework as a foundation for a startup venture company. Nevertheless, the complexity of factors that could influence a startup's future success may necessitate modifications to the valuation framework. Consequently, the valuation framework should be chosen based on the company's current situation and the factors that influence it. Startups with diverse products and businesses, as well as varying valuation frameworks, may employ distinct methodologies and generate diverse results.

In addition, some companies find it necessary to borrow small amounts of seed money from friends, family, and angel investors during the seed or pre-seed phase of investing, while writing a business plan or developing a product prototype. After developing a business plan, companies approach venture capitalists (VCs) for funding [2].

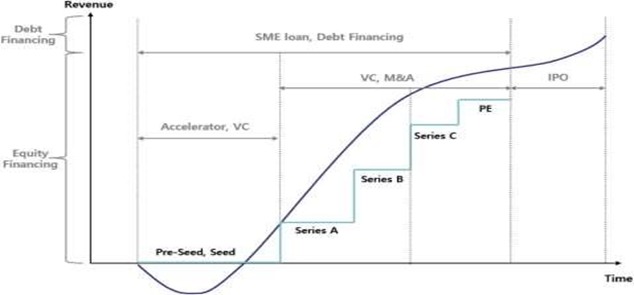

The company aimed to raise sufficient funds for product development in its initial round of venture capital financing. because Research and Development costs are expensive. As companies run out of money, they may seek a second round of venture financing in order to continue working toward the following milestone. The preceding diagram depicts the startup lifecycle from Seed A to Seed B to the final round. The preceding diagram illustrates the revenue and profit positions of the startup company. In addition to obtaining funding, the company employs debt financing and equity financing as part of its strategy.

There are a number of obstacles associated with the valuation of startups. As said by Aswath Damodaran, [3], conducting a corporate valuation is challenging due to the company's historical shortcomings. To have an impact on the valuation of startup assets. Here are some issues with startup company valuations.

First, the financial history of a young company does not have a very limited past. Many of them have only one or two years of financial operations and financing data available. Therefore, it lacks historical financial statements. (Figure 1)

Small or virtually nonexistent business profits. The majority of innovative businesses prioritize the number of users over business profit. Focus more on building a business to increase the volume of transactions than on generating income.

Third, it is dependent upon private equity and venture capital firms. Some startups rely on capital from private sources rather than public marketplaces.

Fourth, many people fail. The occurrence of a startup company achieving Unicorn status in a short period of time inspires other innovators to infuse startup companies with an abundance of innovations. But not all startups succeed and become unicorns. Numerous people have encountered failures and bankruptcies.

The research of [4] Analyzes the variables that impact the valuation of a startup in the context of venture capital (VC). These factors are divided into three categories: startup characteristics, VC characteristics, and external environment characteristics. Startup valuation is determined by industry and location, startup qualities like growth potential, differentiation, and internal procedures, founder and team traits, intellectual property, and strategic alliances.

Multiple founders, a complete management team, past businesses, relevant management, and industry expertise, as well as education level, can increase the valuation of a startup. In addition, previous establishing experience and excellent financial returns from earlier endeavors might result in greater valuations for future businesses. The valuation of a business is also influenced by factors such as intellectual property and strategic partnerships. Moreover, positive blog coverage can act as low-cost marketing for businesses and provide positive signals to VCs [4].

Literature Review

This section discusses the terminology and concepts used in studies employing the Literature Review methodology. It is comprised of seven sections outlining prior research and pertinent case studies taken from journals, books, and papers to support the research.

Characteristics of a Start-Up

Start-up is the first phase of a company's existence. Where a product is typically new and during this phase, the company is focused on developing and refining its product or service, building its team, and establishing a customer base. The value of this company is totally dependent on its potential for future growth. Regarding [3]. Common characteristics of startups include a limited company history, little or no income, a negative cash flow, losses, and a reliance on equity capital. Entrepreneurs and investors confront all of these information constraints when appraising startup businesses.

For a variety of reasons, it is difficult to assign a value It is challenging to designate a valuation for young enterprises or startups. Some are start-ups or businesses based on an idea, with minimal or no revenue and operating losses. Even prosperous startups have short histories, and the majority of startups rely on private finance, ownership savings came first, followed by venture capital and private equity.

The financial life cycle of startups is divided into four rounds based on their principal capital investment requirements: the initial round, round A, round B, and the final round. During the Seed Round phase of a company's development, the founder's ideas and concepts are still being polished. The amount of money a firm will generate is determined by its expected launch expenses.

The majority of entrepreneurs have little to no revenue, and the majority of their expenses are associated with establishing the business as opposed to making money [3]. This combination of limited income and unrelated running expenses typically results in losses and negative cash flow for the majority of new businesses. As a result of initial losses and negative cash flow, companies typically rely on investment capital [3].

Figure 1: by. Hyun & Lee, 2022

The valuation approach for start-ups is distinct. Analysts utilize the existence of intangible assets as a rationale to forsake standard valuation models and build new justifications for investing in nascent companies. The worth of a corporation is still the present value of its expected cash flows from its assets, but these cash flows are notoriously difficult to predict in contrast to startup companies, where cash flow is challenging to predict, the corporation's value is still the present value of the expected cash flow from its assets. valuation methods must identify certain financial factors, such as the company's current financial statements. (Table 1)

A variety of valuation methods can be employed to determine the profitability of a company's investment or the amount it reinvests to generate future development. Typically, these methods involve analyzing all valuation inputs, such as financial statements, market trends, and other pertinent data. A company's revenue and earnings history over time makes it possible to make judgments about how the company's business cycle is and how much growth it shows, while startups don't have those two criteria.

Berkus Method

The Berkus estimates startup value by Scoring the five essential factors of sound idea, prototype, quality of management team, strategic relationship, and sales [6]. There are more qualitative variables involved. Berkus method was discovered by Dave Berkus with the goal of valuing pre-revenue startups. Without focusing on estimated financials, Berkus devised a method for determining the worth of a startup's essential components. In the Berkus method, the factors listed in the table below are considered.

Scorecard Method

The Scorecard conducts a benchmarking process toward the initial value to determine the weighted percent of each 7 key factors, Including, among others, the strength of the management team, the scale of the opportunity, the product or technology,environment,marketing/sales, the competitive and the requirement for additional investment [6].

Risk Factor Summation Method

This method is emphasizes the qualitative attributes of a potential investment. and is therefore closely similar to the Berkus Methodology discussed above, albeit with a broader scope and greater analytical precision [7].

The Risk Factor Summation estimates startup value by adjusting the score of average pre revenue startup valuation in the same region or initial value toward the 12 standard risks faced by early stage company [6].

Each of these 12 factors affects the business model of the venture in the same way. This method is best suited to be complemented by quantitative and qualititative analysis techniques.

Venture Capital Methods

The Venture Capital technique endeavors to extrapolate the actual value of a startup based on an investor's anticipated return at the time of his company withdrawal. This method requires three components for valuation: the size of the investment, the investor's expectations regarding cash use, and an estimate of the startup's exit value [7].

Venture Capital takes account the investor’s point of view as input assumption to estimate the terminal value [6]. Sahlman and Scherlis's venture capital method begins with determining the post-money valuation. Following is the venture capital technique equation:

Return On Investment (ROI) = Terminal or Harvest Value/Post Money Valuation

The First Chicago Method

The Chicago method can be seen as an extension of the discounted cash flow method which is to assess three different scenarios, such as success, survival, and failure.This technique was created in the 1970s by the equity firm First Chicago National Bank and is now extensively employed by venture capitalists. After When designating three scenarios, the present value of each scenario is weighted based on its probability. Mathematically, this can be expressed as follows Venionaire. The First Chicago Method has earned a reputation that has established it as the most popular alternative valuation method in the business world, and is a standard instrument for any standard venture analyst to use on a daily basis.

There have been several previous studies that discussed startup valuation. As research conducted by Destiyana &; Faturohman, [6] , and Dhochak & Doliya, [8], found that several skin valuation that can be used as startup valuation tools consist of Berkus, Risk Factor Summation, and Scorecard.

Regarding research by Miloud et al., [5] Find that strategic management can develop an integrated framework and use input variables crucial to firm performance to directly predict the valuation of a startup business in its early stages.

Different from research conducted by Damodaran & Stern, [4] emphasizes more on how to examine how best to value young companies. Because of the different characteristics shown by startups, it is necessary to determine certain strategies in startup valuation.

Research from Emir Hidayat et al., [8] focuses on determining whether the categories of recent technologies adopted by startups can serve as important valuation factors. The summary below provides information regarding previous research on startup valuation.

Author | Title | Year | Objectives | Finding |

Silva, William Aparecido Maciel Da Fantin, Cristiane Orquisa Fukui, Marcelo Jucá, Michele Nascimento | Startups Valuation: A Bibliometric Analysis and Systematic Literature Review | 2021 | Due to the high levels of uncertainty and risk associated with ventures, identifying funding sources is a pressing matter. | Emphasize the analysis of factors influencing their value at different phases of maturity, as well as the adoption of unconventional valua- tion methods. |

Tarek Miloud, Arild Aspelund, Mathieu Cabrol To | Startup valuation by venture capitalists: an empirical study | 2012 | The article constructs an integrated theoretical framework to examine whether venture capitalists' valuation of a new venture can be explained by factors identified in the strategy theories as being essential to firm performance. | This article finds that the attractiveness of the industry, the quality of the founder and top management team, and external relationships have a significant and positive effect on the valuation of a new venture by venture capitalists when it seeks venture capital financing during its early stages of development. |

Elias Ferraz Cabrera | Venture Capital Valuation Methods: Challenges and Opportunities To Current Trends And Landscape | 2018 | Provide quantifiable standard methodologies indicative of the more stable and consolidated phases of a company's life cycle. | Using reduces the subjectivity of alternative startup valuation approaches for investors. Methods of Venture Capital Valuation |

Dhochak, Monika. Doliya, Prince | Valuation of a startup: Moving towards strategic approaches | 2019 | The referenced study appears to be concerned with the valuation of new ventures and the role of strategic theories in this process. Specifically, the study seeks to determine whether internal-based theory, industry-based theory, and network-based theory can be used to value a new venture and how venture capitalists prioritize and weight these theories when determining the economic value of a new venture. | The results of the study validate the incorporation of strategic variables and provide a systematic method for identifying and measuring the crucial factors when valuing a new venture. |

Aswath Damodaran | Valuing Young, Start-up and Growth Companies: Estimation Issues and Valuation Challenges | 2009 | Determine the optimal method of valuing new businesses. We forecast the company's revenues, earnings, and capital flows using a combination of industry data and the company's own characteristics. | The commonly used approach to venture capital valuation is flawed and should be substituted. |

Sutan Emir Hidayat*, Omar Bamahriz, Nadiah Hidayati, Citra Atrina Sari, Ginanjar Dewandaru | Value drivers of startup valuation from venture capital equity-based investing: A global analysis with a focus on technological factors | 2021 | Examines whether the varieties of recent technologies adopted by startups could serve as significant valuation factors. | The findings suggest that the valuation of startup equity is influenced by a variety of factors, such as financial and nonfinancial information, sectoral differences, and technological differences. |

Figure 2: Theoritical Framework

Research Methodology

To compile the current state of research on the topic for this literature review, we utilized various research search engines, conferences, and scholarly journals. The search is restricted to publications published between 2009 and 2022. Online article searches were conducted using the terms "Startup Valuation Method" and "Value of Valuation method" in the title and keywords of the research database at ScienceDirect, Google Sholar, and Wiley.

The employed methodology is the Preferred Reporting Item for Systematic Reviews. All articles must undergo a selection procedure, after which they are reviewed and summarized based on objective, author's name, publication year, keywords, results, and future research.

Startup valuation Method, Value-Driven during the valuation method are inclusion criteria. Comparing the titles and abstracts of all search results to the criteria is the initial step in the research process.

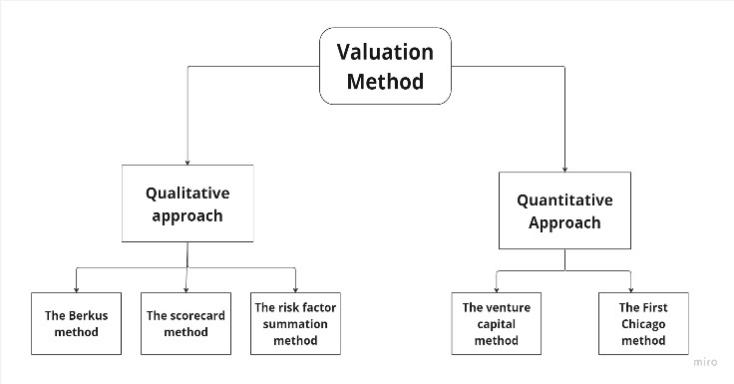

From several explanations related to the method used to conduct startup valuation, it is concluded that startup valuation can be grouped into two, qualitative valuation, which consists of valuation The Berkus method, The risk factor summation method, The scorecard method. In conducting a qualitative approach startup valuation, it is one of the three valuations that can be used.While quantitative consists of the venture capital method and The First Chicago method. The following theoretical framework illustrates the relationship between methods in startup valuation.

The theoretical framework's findings clarify that in assessing startup valuations, multiple methods with two approaches, namely qualitative and quantitative, can be used. Due to the distinct methods for valuing mature companies and startups. Consequently, this method can assist investors in valuing fledgling companies. (Figure 2)

The qualitative method involves evaluation. The Berkus method, the scorecard method, and the risk factor tally method. While quantitative comprises the venture capital and First Chicago methods

The used journal has undergone an identification, screening, and trial process in accordance with the Literature Review method, based on objective research, abstracts, findings, and the journal's potential as a reference journal in the Literature Review. There are six active journals.

It is anticipated that this study will be able to capture how startup companies are evaluated and can be used to examine how startup valuation phenomena occur. The limitation of this study is its generalization of the valuation technique for startups. This can serve as a resource for those investigating the factors and phenomena involved in the valuation of fledgling businesses.

PwC. The Long View: How Will the Global Economic Order Change by 2015? February 2017, http://www.pwc.com/gx/en/world2050/assets/pwc-theworld-in-2050-full-report-feb-2017.pdf.

Hyun, S., and H.S. Lee. “Positive Effects of Portfolio Financing Strategy for Startups.” Economic Analysis and Policy, vol. 74, 2022, pp. 623–633. https://doi.org/10.1016/j.eap.2022.03.017.

Damodaran, A. Valuing Young, Start-Up and Growth Companies: Estimation Issues and Valuation Challenges. Stern School of Business, New York University, May 2009, pp. 1–67.

Miloud, T., et al. “Startup Valuation by Venture Capitalists: An Empirical Study.” Venture Capital, vol. 14, no. 3, 2012, pp. 151–174. https://doi.org/10.1080/13691066.2012.667907.

Destiyana, A.E., and T. Faturohman. “Comparison of Pre-Revenue Startup Valuation Methods.” August 2019, pp. 801–805.

Cabrera, E.F. Venture Capital Valuation Methods: Challenges and Opportunities to Current. June 2019, pp. 1–33.

Dhochak, M., and P. Doliya. “Valuation of a Startup: Moving towards Strategic Approaches.” Journal of Multi-Criteria Decision Analysis, vol. 27, no. 1–2, 2020, pp. 39–49. https://doi.org/10.1002/mcda.1703.

Hidayat, S.E., et al. “Value Drivers of Startup Valuation from Venture Capital Equity-Based Investing: A Global Analysis with a Focus on Technological Factors.” Borsa Istanbul Review, vol. 22, no. 4, 2022, pp. 653–667. https://doi.org/10.1016/j.bir.2021.10.001.