+91 6002993949

submission@himjournals.com

Open Access

ISSN (Print) : 2709-3549

ISSN (Online) : 2709-3557

Until mid-2021, Bank XYZ Syariah not yet has banking services through electronic channels. Due to customer requests, plus the pandemic conditions that limit out-of-branch service, the bank decided to make mobile and internet banking which the bank plan to release at the end of 2021. Before implementing the plan, Bank XYZ Syariah needs to ensure that the investment decisions taken will provide positive financial results for the company in the long term. A study was conducted with two types of tests, a feasibility study using the method of capital budgeting analysis and sensitivity analysis to obtain a clear projection of the financial performance for the next five years. The study results show that the Net Present Value indicator returns positive. The Internal Rate of Return exceeds the Cost of Capital value. The cash flow is projected to return positive in the third year after the investment. In the next step in sensitivity analysis, the calculation identifies four financial factors that are the most sensitive in influencing the financial condition of the project: operating expenses to operating income, effective margin rate, average balance from new customers, and the financing-to-deposit ratio. These four factors have the lowest tolerance level, so it needs special attention from the management to be kept as close as possible to the initial assumptions so that the project's financial condition remains positive. By considering the two test methods, the conclusion that can be drawn is that the mobile and internet banking projects are feasible to continue. Bank XYZ Syariah also needs to set targets for new customers and their average balance and measure pirate metrics related to product effectiveness in customer activation and retention.

Bank XYZ Syariah tends to focus more on financing activities as the primary business because it is typical for their funding customers to not use their accounts for daily transactions. As a result, business funding needs are often not a priority. Such is the case with the mobile banking product, which has not been updated since its creation in 2015.

The Covid-19 pandemic in 2020 has made the need for electronic banking services even more urgent and essential because transactions via branch offices are limited. Hence, customers have no other choice but to use mobile banking. However, the mobile banking performance is minimal because of insufficient investment and maintenance, thus making it difficult for the funding customers (both individuals and corporations) to access their accounts.

In order to solve these business issues, management instructed the bank's funding team to create internet banking products and re-engineer the current mobile banking, which is being developed and will release at the end of 2021. This research intends to assess the feasibility of the company's investment decision to develop both products for the bank's funding customers. The research will also seek to understand which financial factors will significantly impact the project's financial condition.

This study limits the research's result within a five-year time frame and under several financial assumptions, determined by the company's internal data and references from Indonesia's banking industry and economic condition. The analysis method will be based on the calculation results from the data to determine the feasibility of the project using the capital budgeting method and sensitivity analysis.

Capital Budgeting

Capital budgeting is defined in a book titled Principles of Managerial Finance chapter 10 as follows: "The process of evaluating and selecting long-term investments that are consistent with the firm's goal of maximizing owners wealth" [3]. These long - term investments are elaborated in the book titled Capital Budgeting: Financial Appraisal of Investment Projects chapter

1 as "...tangible items such as property, plant or equipment or intangible ones such as new technology, patents or trademarks. Investments in processes such as research, design, development, and testing - through which new technology and new products are created - may also be viewed as investments in intangible assets" [3].

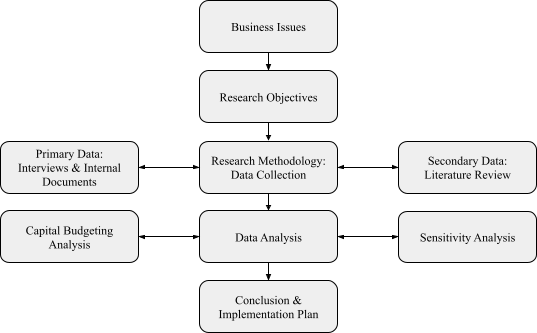

Figure 1: Research Framework

Sensitivity Analysis

Sensitivity analysis is defined in a book titled Fundamentals of Corporate Finance Chapter 11 as follows: "Sensitivity analysis is a variation on scenario analysis that is useful in pinpointing the areas where forecasting risk is especially severe. The basic idea with sensitivity analysis is to freeze all of the variables except one and then see how sensitive our estimate of NPV is to changes in that one variable. Suppose our NPV estimate turns out to be very sensitive to relatively small changes in the projected value of some component of project cash flow. In that case, the forecasting risk associated with that variable is high [9].

Research Design

In this thesis, the quantitative approach is mainly used to assess the development of Bank XYZ Syariah's mobile and internet banking project. The primary data sources are the data projections collected from the internal company document and interviews with the management of Bank XYZ Syariah. The secondary data sources are from academic books or journals related to financial management and the internet. After obtaining the data, the next step is to calculate based on the projections. The calculations will have resulted in capital budgeting indicators for the feasibility study and the acceptable range for each assumption in the sensitivity analysis.

Analysis Method

There are five capital budgeting financial indicators used in this study which are:

Net Present Value: The net present value (NPV) is found by subtracting a project’s initial investment from the present value of its cash inflows discounted at a rate equal to the firm’s cost of capital [3]

Internal Rate of Return: The internal rate of return (IRR) is the discount rate that equates the NPV of an investment opportunity with $0 (because the present value of cash inflows equals the initial investment). It is the rate of return that the firm will earn if it invests in the project and receives the given cash inflows [3]

Payback Period: The payback period is the amount of time required for a firm to recover its initial investment in a project as calculated from cash inflows. Although popular, the payback period is generally viewed as an unsophisticated capital budgeting technique because it does not explicitly consider the time value of money [3]

Discounted Payback Period: One of the shortcomings of the payback period rule was that it ignored time value. The discounted payback period is a variation of the payback period that fixes this particular problem. It is the length of time until the sum of the discounted cash flows is equal to the initial investment [9]

Profitability Index: The present value of an investment’s future cash flows divided by its initial cost [9]

As for the sensitivity analysis result, the study compares the pre-established hypothetical value with the hypothetical value of zero NPV. This study will calculate the size between the two values and shows it as a percentage. A small percentage of change indicates that the particular indicator is very sensitive, with small movements able to reduce NPV to zero or even negative.

This study will limit the revenue estimates based on two income sources: financing margin income and treasury

Table 1: Feasibility Study Result

2021 | 2022 | 2023 | 2024 | 2025 | 2026 | |

Margin Revenue | 34,515 | 49,534 | 109,380 | 293,245 | 539,082 | |

Treasury Revenue | 107 | 154 | 340 | 911 | 1,675 | |

Gross Revenue | 34,622 | 49,688 | 109,720 | 294,156 | 540,757 | |

Operating Expense | (30,600) | (45,474) | (97,744) | (248,803) | (450,902) | |

Marketing Expense | (20,197) | (23,035) | (24,598) | (39,486) | (59,371) | |

EBITDA | (16,175) | (18,821) | (12,622) | 5,867 | 30,485 | |

Depreciation | (2,393) | (2,393) | (2,393) | (2,393) | (2,393) | |

Tax | 0 | 0 | (4,622) | (19,529) | (39,484) | |

Net Income | (18,568) | (21,214) | (19,637) | (16,055) | (11,392) | |

Depreciation | - | 2,393 | 2,393 | 2,393 | 2,393 | 2,393 |

Initial Investment | (13,845) | - | - | - | - | - |

Cash Flow | (13,845) | (7,486) | (2,873) | 18,780 | 71,633 | 142,381 |

PVIF | 1.0000 | 0.8758 | 0.7670 | 0.6718 | 0.5883 | 0.5153 |

PresentValue | (13,845) | (6,556) | (2,203) | 12,616 | 42,144 | 73,364 |

NPV | Rp105,519.88 | |||||

IRR | 76.74% | |||||

Payback Period | 3.08 years | |||||

Discounted Payback Period | 3.24 years | |||||

Profitability Index | 8.62 times | |||||

Table 2: Sensitivity Analysis Result

Sensitivity Rank |

Variable |

Standard | Sensitivity Analysis Result |

Change |

Absolute Change |

1 | Beban Operasional terhadap Pendapatan Operasional (BOPO) | 64.15% | 81.17% |

26.52% |

26.52% |

2 | Effective Margin Rate | 51.00% | 21.00% | -58.81% | 58.81% |

3 | Average balance from the new customers | Rp56.59 |

Rp20.07 |

-64.54% |

64.54% |

4 | Financing-to-Deposit Ratio (FDR) |

97.00% |

33.58% |

-65.38% |

65.38% |

5 | Customer Engagement Cost per Cust (Mio) |

Rp1.50 | Rp4.92 |

228.05% |

228.05% |

6 | Corporate Tax Rate | 22.00% | 88.44% | 302.01% | 302.01% |

7 | Marketing Fee Rate (Y3-Y5) | 6.00% | 25.74% | 329.04% | 329.04% |

8 | Beta | 1.10 | 10.636 | 866.92% | 866.92% |

9 | Marketing Fee Rate (Y1-Y2) | 12.00% | 131.53% | 996.09% | 996.09% |

10 | Inflation Rate | 3.00% | -43.18% | -1539.25% | 1539.25% |

11 | Operation Expense Annual Increase Rate | 10.00% | 284.71% | 2747.09% | 2747.09% |

12 | Customer Activation Cost per New Cust (Mio) | Rp0.10 | Rp4.24 | 4135.91% | 4135.91% |

13 | Corporate Lending Rate/SUN 5 years | 5.13% | -964.71% | -18923.69 % | 18923.69 % |

The net present value (NPV) of Bank XYZ Syariah's mobile and internet banking project returns positive at Rp105,519,881,036, indicating that the project is feasible because the projected cash inflow is more than the projected cash outflow in the next five years. The calculation already includes the concept of the time value of money with a 14.18% discount rate. The internal rate of return (IRR) of Bank XYZ Syariah's mobile and internet banking project is 76.74%, far exceeding the project's 14.18% weighted average cost of capital. This calculation also indicates that the project's likelihood to be profitable is likely.

Based on the payback period indicator, the project is expected to achieve the breakeven point in 3 years and 28 days from the start of the investment period. By that time, the project will recover the investment value from the cash inflows potentially generated from the project. As for the discounted payback period indicator, the breakeven point of the project takes a bit longer in 3 years, two months, and 26 days from the start of the investment period. By that time, the project will recover the investment value from the cash inflows potentially generated from the project after considering the time value of money (TVM) concept.

Based on the profitability index ratio of the project, for every rupiah spent on the project, the potential return on investment is evaluated to be around 8.62 times. Since the ratio is greater than 1, the project is estimated to be profitable and should proceed. From the net profit margin indicators, the project shows negative results in the first two years after the project is launched at -22.81% and -8.02%, but will regain the positive result starting from the third year onwards at 11.24%, 18.25%, and 20.23%.

The sensitivity analysis shows that the most sensitive expense to the project is the BOPO ratio (Beban Operasional terhadap Pendapatan Operasional). This ratio is the most dominant expense, taking around 64.15% of the gross revenue. The ratio should not exceed 81.17%, which will reduce the project's NPV to negative. The current 51% effective margin rate is the second most sensitive metric to the project, as it will determine the revenue generated from the outstanding that the bank manages. Based on the sensitivity analysis, this indicator cannot go lower than 21.00%, which will reduce the project's NPV to negative.

The bank has to set the target to have an average balance of at least Rp20,065,126 from potential new customers as this is the third most sensitive indicator to the project. If the average balance from new customers is less than that, the project’s NPV might turn negative. The fourth most sensitive indicator is the financing-to-deposit ratio (FDR) which currently hovers at around 97%. It means that 97% of the outstanding will be distributed to financing activities. The change in FDR cannot go lower than 33.58%, in which the project's NPV will return negative.

To sum up, the mobile and internet banking project of Bank XYZ Syariah is feasible and predicted to be profitable under several assumptions established. The project should stay feasible if the BOPO ratio, effective margin rate, average balance from the new customers, and financing-to-deposit ratio stay within a specific range, as it will maintain the positive NPV result. Overall, the project is worth the investment because of the potential high profitability for the company in the long run.

Bank Indonesia. Inflation data. https://www.bi.go.id /en/statistik/indikator/data-inflasi.aspx. Accessed 3 Dec. 2021.

Bank Indonesia. Transaksi delivery channel periode 2021. https://www.bi.go.id/id/statistik/ekonomi-keu angan/ssp /transaksi-delivery-channel.aspx. Accessed 29 Nov. 2021.

Damodaran, Aswath. Country default spreads and risk premiums. 8 Jan. 2021, http://pages.stern.nyu.edu/~a damodar/New_ Home_Page/datafile/ctryprem.html. Accessed 2 Dec. 2021.

Dayananda, Don, et al. Capital budgeting: financial appraisal of investment projects. Cambridge University Press, 2002.

Gitman, Lawrence, and Chad Zutter. Principles of managerial finance. Pearson Education Limited, 2015.

Kementerian Keuangan Republik Indonesia. UU 7 Tahun 2021. https://jdih.kemenkeu.go.id/download /a9faab97-aca7-4f87-9fdc-faa8123d1454/7TAHUN2021UU.pdf. Accessed 4 Dec. 2021.

Kristof, Nicholas, and Sheryl WuDunn. "The women’s crusade." The New York Times, 17 Aug. 2009, https://www nytimes.com/ 2009/08/23/magazine/23 Women-t.html. Accessed 2 Oct. 2021.

KSEI. Obligasi Negara Republik Indonesia Seri FR0090. https://www.ksei.co.id/services/registered-securities/government-bonds/lc/FR. Accessed 2 Dec. 2021.

Naja, Hasanul. Modal inti Bank Syariah. Republika, 22 Sept. 2021, https://republika.co.id/berita/qzmc9p457/modal-inti-bank-syariah. Accessed 11 Dec. 2021.

Osterwalder, Alexander, and Yves Pigneur. Business model generation. John Wiley & Sons, 2010.

Ross, Stephen, Randolph Westerfield and Bradford Jordan. Fundamentals of corporate finance. The McGraw-Hill Companies, 2003.

The World Bank. Individuals using the Internet (% of population) – Indonesia. https://data.worldbank.org/indic ator/IT.NET.USER.ZS?locations=ID. Accessed 29 Nov. 2021.

Yahoo Finance. PT Bank BTPN Syariah Tbk (BTPS.JK). https://finance.yahoo.com/quote/BTPS.JK/. Accessed 2 Dec. 2021.

Backer, Gust. The Pirate Funnel. Business Growth Blog, 17 Aug. 2009, https://gustdebacker.com/pirate-funnel-aarrr-framework/. Accessed 10 Dec. 2021.